BY TERRENCE O’BRIEN AND JACK HAMMOND on behalf of themselves and Save Our Super

28 June 2019

When more individuals save for self-funded retirement above Age Pension levels, their savings contribute funds and real resources for reallocation through the financial sector to fund investments. Such an economy will be more dynamic and efficient than one which relies more on incentive-deadening taxes for redistribution through the Age Pension.

Table of contents

Save Our Super suggestions for Review of Retirement Income System

Save Our Super offers the following preliminary ideas for the Review of the Retirement Income System. We regard such a review as highly desirable and potentially path-breaking if well directed, but fraught with dangers for the Government and threatened with futility if not properly handled.

1. Embed a clear statement of Government retirement income objectives in the Review’s Terms of Reference

The Superannuation (Objective ) Bill 2016 attempted to legislate an objective for superannuation, as if that would somehow guide future governments’ detailed regulatory and tax decisions for superannuation. It did not identify the objective for the Age Pension, nor explain how the two elements ought to interact in the overall retirement income system.

Both Save Our Super and the Institute of Public Affairs criticised that attempt, and suggested improvements.

The effort to define objectives is much better set in the broader retirement income framework now envisaged.

Saving is a contested issue of philosophical vision.

To most Australians, saving is the process by which those prepared to delay gratification and consumption make real resources available to those with an immediate need for them. Savings are not just a pile of money that Scrooges sit over and count. From the dawn of history, when families saved some of autumn’s grain to provide seed for next spring’s planting, saving in every culture has been the means by which living standards have grown and the next generation has been given more opportunities than their parents.

Saving funds investment. In the modern economy, it provides both the finance and, indirectly, the real resources that are allocated through capital markets to the businesses or loans that produce the biggest increase in the community’s living standards. If Australian investment cannot be financed by Australian saving (either by households, companies or governments running budget surpluses), it has to be financed by borrowing from foreigners or accepting direct foreign investment in Australian projects.

Viewed against that backdrop, household saving is good. Raising household savings, just like eliminating government budget deficits (ie stopping government dis-saving), reduces Australian reliance on selling off assets to foreigners or contracting foreign borrowing. People should be able to save as much as they wish, ideally in a stable government spending, taxation and regulatory structure that does not penalise savings or distort choice among forms of saving. In such an ideal framework, they should be allowed to save for retirement, for gifts, for endowments, for bequests or for any purpose for which they choose to forgo consumption.

Specific tax treatment of long term saving (such as capital gains tax, and tax treatment of the home and superannuation) is necessary to reduce the discouragement to saving from government social expenditures and from levying income tax at rising marginal rates on the nominal returns on saving. But critics regard such specific treatment as ‘concessions’ to be reduced or eliminated. They want to limit what saving can occur, and tax what does occur. Critics think of private saving not as the foundation of investment, but as the wellspring of privilege and intergenerational inequity.

We suggest the Terms of Reference for the Review should in its preamble set the Government’s practical and philosophical aspirations for household saving and the retirement income system. We suggest the preamble to the Terms of Reference should highlight:

- The retirement income system as a whole should aim to ensure that as the community gets richer, retirees should through their own saving efforts over a working lifetime, both contribute to and share in those rising community living standards.

- The Age Pension should be focussed as a safety net for those unable to provide for themselves in retirement because of inadequate periods in the workforce or otherwise limited earnings and saving opportunities.

- As the population ages, superannuation saving for retirement is likely to be a growing part of the national savings effort. Buoyant growth in superannuation finances investment and lending, and helps support rising living standards. (Conversely, a rising dependence on the Age Pension would spell only a higher tax burden).

- The design of the retirement income system must be:

- stable;

- set on the basis of published, contestable modelling; and

- evaluated for the long term, namely, the 40 or so years over which lifetime savings build, and the 30 or so years in which retirees can aspire to enjoy whatever living standards they have saved for.

- The Age Pension and superannuation systems and the stock of retirement savings should be protected as far as practicable by grandfathering assurances against capricious adverse changes in future policy. Such changes create uncertainty and destroy trust in saving and self-provision for retirement.

2. Avoid policy prescription of savings targets or permissible retirement income standards

Some commentators have proposed the idea of a ‘soft ceiling’ on levels of retirement income saving acceptable to policy. That approach derives a level of acceptable retirement income by working backwards from the observed historical pattern of retirees’ spending, which declines with age, especially after age 80. According to those views, the fact that some retirees continue to save even after retirement is regarded as a sign of policy failure and excessively generous tax treatment (rather than of recently rising asset values). Saving is treated, in effect, as allowable to those of working age, but to be discouraged beyond a certain point, and prevented for retirees. According to this analysis, we already have “more than enough” money in retirement.

The Grattan Institute suggests a savings target such that all but the top 20 per cent of workers in the earnings distribution achieve a retirement income of 70 per cent of their pre-retirement income over the last five years of their working lives. For those in the top 10 per cent of the earnings distribution, a replacement rate of 50-60 per cent of pre-retirement earnings is “deemed appropriate”. (Approved retirement income for the second decile is not specified.)

Even after discouraging saving in this way, Grattan also recommends the introduction of inheritance taxes.

The Terms of Reference should make it clear that the Government does not support such ideas. It should emphasise it regards saving for retirement as beneficial to the community, and does not wish to limit it by arbitrary targets.

3. Prevent another ‘Mediscare’

Possible changes to the Age Pension, its means tests, compulsory superannuation contributions, superannuation taxation or regulation will be inevitably contested.

There is now zero public trust in the stability and predictability of retirement income policy. That results from the reversal, in 2017, of Age Pension and superannuation policies which, after extensive research and consultation, were introduced as recently as 2007. In addition, public trust has been eroded by the 2019 Labor election platform to make wide-ranging increases in taxes on long-term savings (that is, the Capital Gains Tax, franking credit and negative gearing proposals).

No other area of policy has more complex interactions and regulations from policy changes than the retirement income field. Complexity is such that legions of financial planners specialise in advice on the interaction of income tax, superannuation, the Age Pension and aged care arrangements.

No other area of policy takes longer lead times (40-plus years) to produce the full effect of policy change, and has the capacity to impose irrecoverable losses in living standards on vulnerable people that they can do nothing to manage or avoid. People, late in their working career or those already retired, are rightly extremely cautious about policy-induced reductions in retirement living standards they have long saved towards. It is easy for political opportunists to exploit that caution.

No review of policy will get to first base if it can be misrepresented by political opponents as creating uncertainty, destroying lifetime saving plans or retirement living standards. Given recent experience, many voters are understandably receptive to a fear campaign of misrepresentation, including those forced to make compulsory savings throughout their working life; those dependent on the full or part Age Pension; wholly or partially self-funded retirees; and indeed all those presently retired, close to retirement, or those who have responded lawfully to legislated incentives to save as previous governments intended. If aroused to uncertainty, these groups can destroy a government.

Many of the changes that would usefully be addressed by a review of retirement income policy are potentially political third rail issues if poorly handled. To take just one example, consider how the family home is treated under the Age Pension asset test and in the structure of Age Pension payments. Think tanks of the left and right alike have recommended that treatment be changed to take more account of wealth in the family home. Without insurance against ‘Mediscare’-type attacks, a potentially important avenue of reform would instantly be used as a scare. Government would have to either instantly rule out any change (compromising the review) or watch the reform exercise die while still suffering the political fallout as ‘the party that wants to tax your home’.

So even sensible proposed changes in policy would be discounted as untrustworthy, disruptive and unlikely to endure without careful protections. No assurance by any political party that “it is not intending to make any change” will be believed for a minute. However, these problems are avoidable with the good management sketched below.

4. Disarm scaremongering by an absolute, up-front guarantee of grandfathering

The simple, tried and proven way to disarm the ‘Mediscare’ tactic and ensure an open, constructive and intelligent Review is to make an upfront, unconditional guarantee: the Review of retirement income will be instructed to avoid any recommendations which would significantly adversely affect anybody who has made lawful savings for retirement, and who is presently retired, or too close to retirement to make offsetting changes to their life savings plans.

That grandfathering guarantee should be absolute and unconditional, referring to the use of similar practices in Australia’s history of superannuation changes from the Asprey report in 1975 through to 2010. The force of any guarantee would be increased if the Government now grandfathered some or all of the 2017 measures initially introduced without grandfathering, in the manner discussed below.

Such unconditional grandfathering would not destroy the retirement income, economic or fiscal benefits of undertaking reform. The very reason that retirement income policy changes take a long time to have their full effect is a good reason for starting policy change early, grandfathering those who made their retirement income savings under earlier rules to ensure implementation of the reforms, and letting the benefits of reform build slowly over time.

5. Propose means to rebuild and preserve confidence and trust in future consideration of retirement income policy changes

Recent policy design efforts have tried to encourage new superannuation products, such as those to address longevity risk. But such effort, necessarily focussed on the distant future of individuals’ retirements, is futile if no one trusts superannuation and Age Pension rule-making any more. If savers cannot trust the Government from 2007 to 2017, or even from February 2016 to May 2016, why should they trust the taxation or regulation of products affecting their retirement living standards 40 years in the future?

To restore the credibility of any changes emerging from the Review, the terms of reference should encourage renewed examination of ideas such as the superannuation charter recommended by the Jeremy Cooper Charter Group, or possible constitutional protection of long term savings and key parameters of the retirement income system.

6. Rebuild credible public, contestable, long-term modelling of the effects of change on retirement incomes

Retirement incomes are the result of complex and slowly developing interrelationships between demographic change, growing community incomes, rising savings, government budget developments, and Age Pension and superannuation policies. Formal, published, long-term modelling of these relationships is an essential tool to understand the impact of demographic change and of policy settings. Formal modelling facilitates public understanding and meaningful consultation, and helps build support for future retirement income reform. Such public modelling was integral to the development of the Simplified Superannuation package in 2006, implemented from 1 July 2007, but was lacking from the 2017 reversal of those reforms.

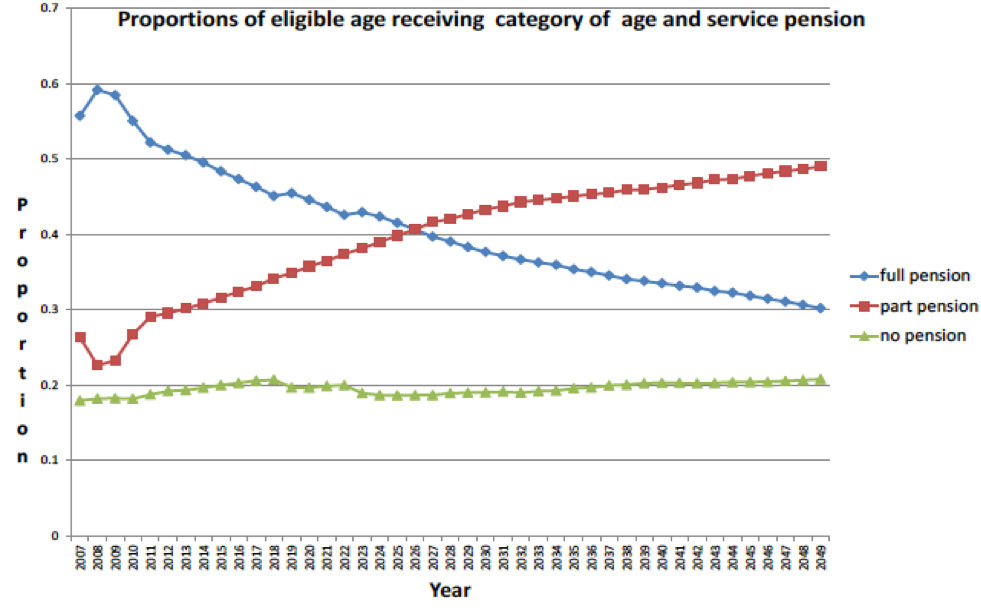

In about 2012, the Commonwealth Treasury stopped publishing long-term modelling in this field with the last of its published forecasts using the RIMGROUP cohort model. The then-projected impacts on the Age Pension through to 2049 from the Super Guarantee measures of 1992 and the Simplified Superannuation reforms of 2007 were for a large decline in uptake of the full Age Pension accelerating from about 2010, but an increase in the uptake of part Age Pensions. There was projected to be only a small rise in the proportion of those age-eligible for the Age Pension who were fully self-funded retirees (Chart One).

The reason that the projected growth in self-funded retirement was slow is instructive: people who would, on pre-2007 policies, have been eligible for a full Age Pension could only slowly build their superannuation savings in response to the 2007 changes. Some of the first cohorts reaching retirement age would have sufficiently larger superannuation savings to be ineligible for the full Age Pension, but would still be eligible for a part Age Pension. Moreover, as they aged and exhausted modest superannuation savings, they would become eligible for a full Age Pension in later life.

Chart One: Treasury’s 2012 projected changes in pension-assisted and self-financed retirement, 2007-2049

Source: Rothman. G. P., Modelling the Sustainability of Australia’s Retirement Income System, July 2012.

The 2017 reversals of the 2007 reforms have never been properly justified. There was no published modelling to suggest costs to the budget were higher than projected, or transition to higher self-funded retirement incomes was slower than projected. As Save Our Super warned at the time, the 1 January 2017 increased taper on the Age Pension asset test created a ‘death zone’ for retirement savings between about $400,000 and $1,050,000 for a couple who owned their home. For every extra dollar saved in that range, an effective marginal tax rate of up to 150 per cent sent the couple backward. (Similar death zones arise for other household types and single persons.)

Superannuation balances at retirement for males of $400,000 or more are common, so the practical burden of the 1 January 2017 perverse de facto tax increase could only be mitigated if a saver could quickly traverse the death zone through utilising high concessional and non-concessional contributions to accelerate late-career super savings. But then the 1 July 2017 reductions in superannuation contribution limits scotched that hope, and compounded the damage of the 1 January 2017 change.

The longer those perverse 2017 incentives are left to operate, the stronger the incentives to build a retirement strategy around limiting superannuation savings and maximising access to a (substantial) part Age Pension. That will negate the objective of the Howard/Costello reforms to defeat adverse demographic budgetary impacts by encouraging rising self-funded retirement, growth in retirement living standards and reduced use of the Age Pension.

Outsiders will probably never know how the policy advice to make the 2017 policy reversal arose, but we speculate that the failure to publish long-term, contestable modelling since 2012 contributed to policies perversely destructive of retirement savings and encouraging tactical exploitation of access to the part Age Pension.

7. Highlight accelerated success in retirement income policy

As a result of the policies that applied up to 2017, we were witnessing a remarkable evolution of Australian retirement income outcomes that is passing unnoticed, because it is poorly explained and reported, and its end-point is still decades in the future. The combined effects of the 1992 Superannuation Guarantee process and 2007’s Simplified Superannuation are beginning to strongly reduce expenditures on the Age Pension much faster than was earlier projected.

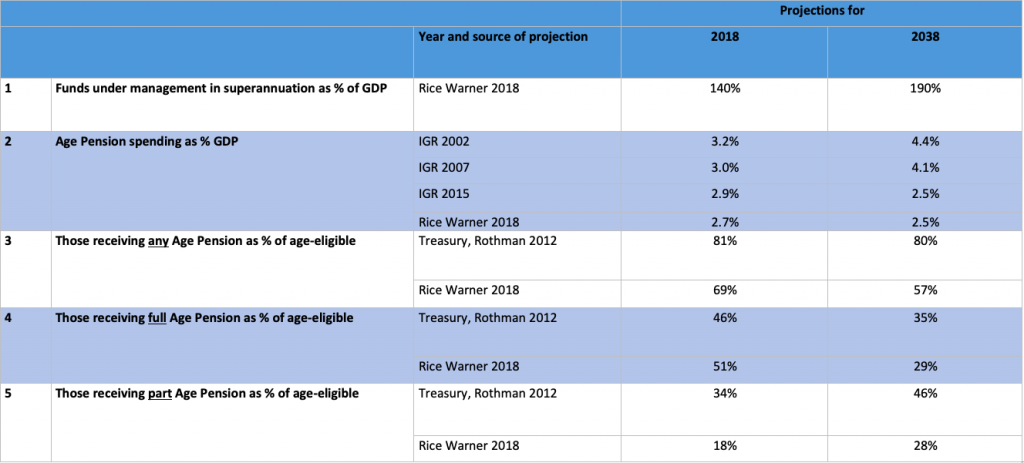

The most recent projections of retirement developments, though only for 20 years out to 2038, were published in 2018 by Michael Rice for Rice Warner actuaries: The Age Pension in the 21st Century. (Treasury had a team leader on secondment to Rice Warner’s team of actuaries for the exercise.) The current trends are remarkable in themselves, but more remarkable in contrast to previous projections of how growing superannuation savings were changing the take-up of the Age Pension only slowly.

The proportion of those age-eligible for the Age Pension who draw a part Age Pension is still rising. (That growth comes from those previously eligible for a full age pension but now partly self-financing their retirement. So there is a net saving to the budget from this trend). But the rise in the take up of the part Age Pension is not as much as earlier projected (Table 1, Panel 5).

What was originally projected to be only a very slight decline in the proportion of the age-eligible receiving any Age Pension (from 81 per cent in 2018 to 80 per cent by 2038), now looks likely to be a very large decline, to about 57 per cent (Table One, Panel 3, and Chart Two).

Table One: Rapid decline in Age Pension uptake projected to 2038

Notes: Intergenerational Report projections quoted are for years closest to 2018 and 2038. 2018 numbers were projections where earlier reports are cited, but are estimates of current data where a 2018 source is cited.

Sources: Intergenerational Reports for 2002, 2007 and 2015; Rothman. G. P., Modelling the Sustainability of Australia’s Retirement Income System, July 2012 (published again in the Cooper Report, A Super Charter: fewer changes, better outcomes, 2013); Rice, M., The Age Pension in the 21st Century, Rice Warner, 2018; Roddan, M., Pension bill falling as super grows, Treasury’s MARIA modelling shows, The Australian, 24 March 2019.

Put the other way around, the proportion of those age-eligible for the Age Pension who are instead totally self-funded retirees will have risen from some 31 per cent in 2018 to about 43 percent in 2038. This is a 12 percentage point rise in those totally self-funding, instead of the earlier projected 1 percentage point rise.

Reflecting this continuing gradual maturation of the system as it stood up to the 2017 policy reversals, spending on the Age Pension has already commenced declining as a share of GDP, instead of rising significantly as had been projected in early Intergenerational Reports. By 2038, spending on the Age Pension will be almost 2 percentage points of GDP lower than originally projected in the first Intergenerational Report in 2002.

Projections will doubtless evolve further. But the remarkable trends noted here are already surprising those working with current expenditure data. The December 2018-19 Mid-Year Economic and Fiscal Outlook noted spending on the Age Pension had been overestimated by $900 million for reasons yet to be fully understood. The shortfall seems likely to involve the trends noted here, among other factors.

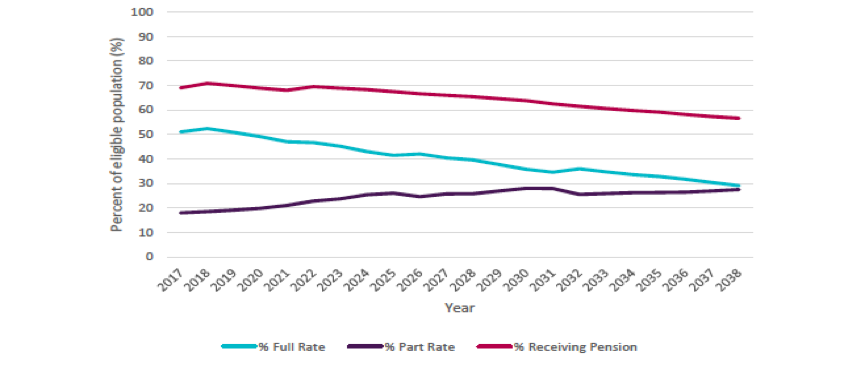

Chart Two: 2018 Projected proportions of the eligible population receiving the Age Pension, by rate of Age Pension

Source: Michael Rice, The Age Pension in the 21st Century, Rice Warner, p 31.

To most, the evidence of rising living standards in retirement, more self-funding through lifetime savings, less reliance on the Age Pension, a falling share of Age Pension spending in GDP and the disarming of the demographic and fiscal time bombs identified in earlier Intergenerational Reports would look like a policy triumph.

Further to this private sector modelling, in December 2018, an FOI request led to the first fragmentary public evidence of the initial uses of a new Treasury microsimulation model, MARIA , a “Model of Australian Retirement Incomes and Assets”. The model uses advances in data and computing power since Treasury’s 1990s RIMGROUP model was built to move from cohort modelling of age and income groups to microsimulation modelling of the population. This first report indicated Age Pension dependency falling markedly. Subsequent reporting of FOI information in March 2019 adds to public information that spending on the Age Pension is now falling towards 2.5% of GDP by 2038, a remarkable 1.6 per cent of GDP lower than was projected in the Intergenerational Report of 2007, the year the Costello Simplified Super reforms were enacted.

To give a sense of scale, 1.6 per cent of 2018 GDP is about $29 billion dollars. Even if GDP grew by 1% a year to 2038 (which would be a lamentable shrinkage in per capita GDP), spending on the Age Pension would be by then about $36 billion a year lower than previously projected, apparently wholly as a result of more people saving more in superannuation than was projected in the Intergenerational Report of 2007.

On 24 June 2019, more evidence of superannuation policy success became available. Analysis by Challenger, Super is delivering for those about to retire, noted that the average newly retired Australian is not accessing the Age Pension at all. Only 45% of 66-year-olds were accessing the Age Pension at December 2018 and only 25% of them were drawing a full Age Pension. Of course, many of those might fall back on the Age Pension in later life when they exhaust their superannuation capital. Thus, if retirees are to remain wholly self-funded during their whole retirement, superannuation balances at retirement will need to keep rising. Other things being equal, 2017’s imposition of a $1.6 million cap and tax at 15% on amounts above that balance reduce the time that retirees can remain independent of the Age Pension.

Every additional person who wholly self-funds their retirement is, prima facie, achieving a better retirement living standard than they could have enjoyed by arranging their affairs to access only the Age Pension and to send the bill to working age taxpayers. This is not merely a budget success. An economy in which individuals save for retirement, contributing funds and real resources for reallocation through the financial sector to fund investments will be much more dynamic and efficient than one more dependent on the Age Pension, in which people pay incentive-deadening taxes for redistribution through the welfare system.

It is bewildering to us that the accelerated success of superannuation policy, which has helped people save for their desired retirement standard of living, is not being trumpeted from the rooftops. Instead, the facts are dribbling out without explanation and context from FOI applications. Those facts are lost against the backdrop of incessant criticism from some commentators of More than enough saving and excessive revenue forgone from the tax treatment of superannuation.

It is vital for protecting the Government from a repeat of the backward steps on retirement income policy in 2017, for restoring the legacy of the Howard-Costello reforms and for timely identification of sustainable future reforms, to re-establish regular published, contestable and peer reviewed modelling of how retirement income policy is working.

8. Commission initial modelling of three scenarios

We suggest Treasury should use MARIA to model three scenarios over a long-term time frame such as 2000 to 2060 to clarify the starting point for the Review of Retirement Income Policy.

Rather than study retirement income policy solely as a Commonwealth budget issue of the revenue hypothetically forgone in tax incentives for superannuation and the expenditure on the Age Pension, the modelling needs to be set in the fuller context of the Howard Government’s 2006-2007 analysis of Simplified Superannuation. Its output ought to include impacts on retirement incomes, the ‘RI’ in MARIA, not just on the budget.

As noted above, the overarching objective of policy ought be to enable higher lifetime saving and rising living standards in retirement for those in a position to save for self-funded retirement, while preserving the Age Pension as a safety net for those unable to save for a better retirement living standard. Modelling should project implications for average self-financed and Age Pension retirement incomes under each scenario, as well as for government revenues and expenditures.

a) A baseline scenario

We suggest the first scenario for long-term modelling should be the projected effects by 2060 of the continuation of Age Pension and superannuation policies as at end 2016. That would be comparable against the earlier 2012 Treasury modelling, and would show the impact of another 6 to 7 years’ data on the maturation of the Super Guarantee (including scheduled future increases) and the Simplified Superannuation reforms of 2007.

b) A current policy scenario

We suggest a second useful scenario would be to model the current policies. When the current policy scenario is compared to the baseline scenario, that would give an indication of the effect of the change in the taper rate of the Age Pension asset test, the imposition in the retirement phase of a 15% tax on earnings on superannuation balances above $1.6 million, and tighter restrictions on concessional and non-concessional contributions. Effects on individual retirement incomes, as well as comparisons of effectson government revenue and expenditure over time, should be made between the two models.

It might be objected that the behavioural responses to the 2017 changes are too recent to have shown up in data and thus too difficult to model. But to assert that we can have no estimate of the likely effect of those policy changes on retirement incomes would be in effect to concede that they should never have been proposed or implemented.

c) Future policy change scenarios

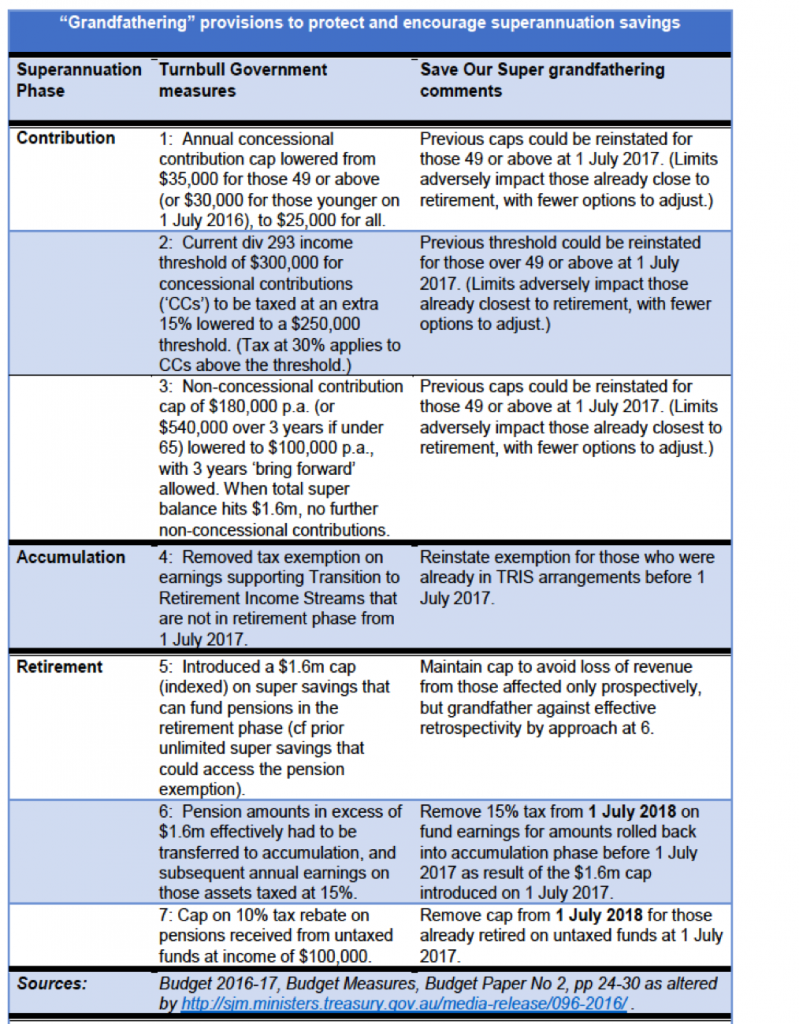

A third useful scenario could involve empirically testing policy changes the Government wanted to explore, including grandfathering the changes introduced in 2017 and summarised in Table Two.

Any mix of measures selected should cohere around the Government’s retirement income strategy, to allow those who can save to raise their retirement living standards, to protect the efficacy and affordability of the Age Pension as a safety net for those who cannot, and to ensure as many as possible are in the first group. The selection of measures must rest on the evidence of public, contestable, long-term modelling of outcomes on both retirement living standards and the government budget.

Because of these strategic and empirical imperatives, Save Our Super advocates that the grandfathering of all the measures of Table Two be enumerated and modelled, as well as the 2017 change to the means testing of the Age Pension and the impact of Superannuation Guarantee changes.

Table Two: Options for grandfathering 2017 superannuation changes

We illustrate one possible, strategically coherent path forward but without any implied prioritisation. Some potentially useful measures might:

- Reduce the burden of the Superannuation Guarantee on the youngest (who have longest to fund their own preferred retirement living standards and face the highest competing demands on their early-career budgets) and the poorest (who will in any event accumulate insufficient savings over their working lifetimes to become ineligible for the Age Pension). This could involve either raising the cut-in point for the Superannuation Guarantee, halting its programmed rate increases, or both.

- Against the merits of the Superannuation Guarantee must be set the cost that it forces a constant rate of saving for employees by their employers over the employees’ working lifetimes. In any event (but especially if the Government raises the Superannuation Guarantee rate), this is a particular burden on the young, those in tertiary study, those seeking to buy their first home, those establishing a family and those with low or punctuated career earnings.

- One curious and little noted feature of the Superannuation Guarantee is that (broadly speaking) it applies to any employee over 18 who earns $450 gross or more a month. This extraordinarily low threshold has not been altered since the Super Guarantee was introduced at 3 per cent in 1992 – over a quarter of a century ago. At that time, the monthly $450 trigger corresponded to the then annual tax-free threshold in the income tax of $5,400. With the Superannuation Guarantee now at 9.5 per cent and scheduled to increase to 12 per cent, it is now a significant impost that falls as forgone wages on young and/or poor workers, when they have priorities of education, housing and family expenses much more pressing than commencing saving for retirement more than 40 years in the future. If the Superannuation Guarantee cut in at the monthly gross earnings equivalent to the current tax-free threshold, the trigger would now be $1517 a month, not $450 a month.

- Remove the discouragement of saving from effective marginal tax rates of over 100%, encouraging saving by those who can save to escape reliance on the full Age Pension. This would require reversing the increased taper on the Age Pension asset test imposed on 1 January 2017 and reinstating the Costello reform of 2007.

- Allow those who are able to save for their desired retirement standard of living, in the latter parts of their career, access to higher concessional and non-concessional superannuation contributionlimits, as shown in Table Two.

- Acknowledge that self-funding a retirement standard of living which is higher than the Age Pension requires a large capital sum at retirement – the Age Pension for a married couple is estimated to have an actuarial value of over $1 million, with the costs rising in an environment of near-zero interest rates. At present, all political parties say they want an end (increased self-funding of retirement), but seem to attack the means to that end: a large capital sum accumulated at the end of the saver’s working career. With the continuing drift of interest rates towards zero, whatever unexplained calculations arrived in 2016 at the $1.6 million cap on superannuation should be re-examined, with a view to grandfathering the cap as shown in Table Two, raising it or abolishing it. The interest earnings from a $1.6 million sum is now almost 40% lower than it was in early 2016. Abolishing the $1.6 million cap would re-capture many of the simplification benefits of the 2007 Simplified Super reforms, which were destroyed by the 2017 changes.

d) Strategic direction of future policy change scenario

These four classes of change have clear strategic directions: they are pro-choice, pro-personal responsibility and support rising living standards in retirement. They reduce emphasis on forced savings at a high and constant rate over the whole of working life from the earliest age and the lowest of incomes. They increase emphasis on saving at the rate chosen by individuals over their working careers in the light of their circumstances. The shift would likely result in faster late career savings after educational, family formation and mortgage commitments have been met. The shift would be pro-equity, in that it would avoid reducing the living standards of the youngest and poorest in the workforce, without ever helping many of them achieve retirement income living standards above the Age Pension. And it would reduce the constituency of voters denied growth in their own disposable incomes and supportive instead of increased government transfers to them for their early-career expenditures (such as childcare and other family benefits).

e) Budget effects of future policy change scenario

Of these four classes of change, the Superannuation Guarantee changes would raise significant revenue for the government budget, since higher incomes paid as wages would be taxed under normal income tax provisions, rather than at the lower rate for superannuation contributions. The other three measures would have a gross cost to budget revenue relative to the current measures, but would continue and likely accelerate the recent and faster-than-projected exit of retirees from dependence on the full Age Pension. That will save some future budget outlays, and it is unclear until public, contestable long-term modelling is published what the net effect on the budget would be, and its time frame.

Recall, however, that the origins of this debate were the demographic time-bomb facing Australia, and the intrinsically long-term challenge of building life-time savings for long-lived retirement. A measure that ‘breaks into the black’ even decades hence might be counted a success.

f) Retirement income effects of future policy change scenario

Whatever the net budget effects and their timing, it is clear a package such as sketched in scenario 3 will raise Australian’s retirement incomes and protect the sustainability of the Age Pension

9. Let the modelling speak

Only long-term modelling can show which measures are likely to have the best pay-offs in greatest retirement income improvements at least budget cost. Choice of which measures to develop further are matters for judgement, balancing the possible downside that extensive policy change outside a superannuation charter may only further damage trust in retirement income policy setting and in Government credibility.

*******************************************************

1 ping

[…] Save Our Super suggestions for Review of Retirement Income System […]