Aaron Hammond

Author's posts

The new ‘ipso facto’ regime and SMSFs

Joseph Cheung (jcheung@dbalawyers.com.au), Lawyer and Daniel Butler (dbutler@dbalawyers.com.au), Director, DBA Lawyers

The new law pertaining to ‘ipso facto’ clauses came into operation on 1 July 2018. This article highlights the relevance of the new law for SMSFs. Note that the law in this area is complex and a detailed and careful analysis is required to properly understand how the new ‘ipso facto’ regime operates.

Background: Purpose of the new law

‘Ipso facto’ is a Latin phrase that means ‘by the fact itself’. An ‘ipso facto’ clause is a provision in a contract that allows one party to terminate or modify the operation of a contract upon the occurrence of some specific event, regardless of otherwise continued performance of the counterparty. For example, in an insolvency context, a clause in a lease that allows one party to terminate the lease if the counterparty enters into external administration is an ‘ipso facto’ clause.

For the counterparty that is affected by an insolvency or formal restructure process, some negative consequences of ‘ipso facto’ clauses include (but are not limited to) the following:

- the ability to successfully restructure could be reduced; or

- the market value of a business entering formal administration could be destroyed; or

- the business could be prevented from being sold as a going concern.

The introduction of the new law relating to ‘ipso facto’ clauses is part of the Federal government’s reform of Australia’s insolvency laws. This new law is aimed at enabling businesses to continue to trade in order to recover from an insolvency event.

Summary of the new law

Broadly, this new law applies to contracts entered into on or after 1 July 2018 and makes certain ‘ipso facto’ clauses that amend or terminate a contract unenforceable if the ‘ipso facto’ clause is triggered merely because:

- the company is entering into administration (Corporations Act 2001 (Cth) (‘CA’) s 451E) ; or

- a managing controller has been appointed over all or substantially all of a corporation’s property (CA s 434J); or

- the company is applying for or undertaking a compromise or arrangement for the purpose of avoiding being wound up in insolvency (CA s 415D).

Generally, where a triggering event under any of the abovementioned three categories occurs, there is a ‘stay on enforcing rights’. Please note that there is further detail in each relevant section of the CA, covering aspects such as the timing of the stay and the Court’s ability to extend the period of the stay. However, a detailed examination of these sections is beyond the scope and purpose of this article.

Note also that there also exists exceptions to a ‘stay on enforcing rights’. We summarise these exceptions into four categories:

1 The right is a right under a contract, agreement or arrangement entered into after a triggering event.

2 The right is contained in a kind of contract, agreement or arrangement that is prescribed by the regulations or a kind declared by the Minister.

3 The right is a right of a kind declared by the Minister.

4 Certain parties (named in the CA) have consented in writing to the enforcement of the right.

Where a party wishes to enforce their rights despite a stay, they can apply for a court order. Broadly, the Court may issue an order if the Court is satisfied that this is appropriate in the interests of justice. (Refer to the CA ss 415E, 434K, 451F for further details about the criteria that the Court considers before making an order).

Despite the operation of a ‘stay on enforcing rights’, the new law does not prohibit the exercise of a right for any other reason. For example, where there is a breach involving non-payment or non-performance by one party, the counterparty party can pursue its legal rights.

Relevance of the new law for SMSFs

While the new law relating to ‘ipso facto’ clauses is not specifically targeted at SMSFs, it is relevant since there are an increasing number of SMSFs, especially SMSFs with corporate trustees, and these SMSFs often enter into various contracts that may contain ‘ipso facto’ clauses. The following are some common scenarios:

1 An SMSF owns business real property and leases it to either an unrelated third-party tenant or a related party tenant. A lease agreement is executed by the SMSF as lessor.

2 An SMSF invests by providing a loan to an unrelated third-party borrower. A loan agreement is executed by the SMSF as the lender.

3 An SMSF enters into a limited recourse borrowing arrangement (‘LRBA’) to purchase real property. The SMSF executes a loan agreement in its capacity as the borrower. The custodian/bare trustee company might also be included as party to the loan agreement.

Naturally, there are many other scenarios where an SMSF may enter into a contract.

In the first scenario, the lease may contain provisions stating that the lease agreement is terminated if the tenant enters into administration or the tenant fails to make a lease payment within a prescribed time period. Similarly, in the second scenario, the loan agreement may contain provisions stating that the loan agreement is terminated if the borrower enters into administration or the borrower fails to make a loan repayment within a prescribed time period. In both the first and second scenarios, the SMSF trustee may seek to rely on these provisions to terminate the agreement with the other party on the occurrence of a triggering event.

In the third scenario, the LRBA documents may contain provisions stating that the loan agreement is terminated if a certain triggering events occur, such as if the SMSF trustee enters into administration or the SMSF trustee fails to make a loan repayment within a prescribed time period. In the third scenario, the third party may try to rely on the provisions against the SMSF trustee upon the occurrence of a triggering event. In all three scenarios, there may be other clauses that deal with the consequence of the termination. It is important for SMSF trustees and advisers to know whether such clauses can be relied upon if a certain triggering event occurs. In certain circumstances, they may also have to decide whether any documents need to be updated in light of the new law relating to ‘ipso facto’ clauses.

The following is a brief checklist of questions for SMSF trustees and advisers to consider when reviewing contracts.

1 Is a certain clause in the contract an ‘ipso facto’ clause? For example, a clause stating that the contract is amended / terminated if the borrower enters into administration is most likely an ‘ipso facto’ clause.

2 If the clause in the contract is an ‘ipso facto’ clause, does an exception apply? Consider whether the right falls within one of the four categories of exceptions. If an exception applies, there is no ‘stay on enforcing rights’, and the relevant party can seek to rely on the ‘ipso facto’ clause to amend / terminate the contract.

3 If an exception applies and there is a ‘stay on enforcing rights’, can another clause be relied upon for the amendment / termination of the contract? For example, if the borrower has entered into administration and has also failed to make a loan repayment on time, the lender (ie, the SMSF trustee) may seek to terminate the loan agreement. A clause that states that the loan is terminated if the borrower enters into administration may be an ‘ipso facto’ clause and the lender may be prohibited from enforcing a right to terminate based on this fact. However, there may be another clause that states that any outstanding moneys can be recovered if a payment is not received on time. Further, the loan agreement may also specify that the full amount of the loan becomes payable if the borrower fails to make a loan repayment within the prescribed time period. This could allow the lender to recover the full loan amount plus interest plus costs, and to effectively bring the loan agreement to an end despite the other ‘ipso facto’ clause. Such a clause could protect the SMSF trustee in its capacity as a lender.

For completeness, please note that a ‘stay on enforcing rights’ relating to an ‘ipso facto’ clause does not by itself invalidate a contract. Furthermore, the law in relation to ‘ipso facto’ clauses may be subject to further change in the future. For example, the exceptions to ‘stay on enforcing rights’ may change, so it is prudent to review the law on a regular basis.

Conclusion

SMSF trustees and advisers should review all contracts entered into on or after 1 July 2018. SMSF trustees should also obtain documentation (such as LRBA documentation) from a quality supplier firm that has reviewed its documentation to ensure that it is up-to-date in light of this new law in relation to ‘ipso facto’ clauses.

The law in relation to ‘ipso facto’ clauses is a new area of law and where in doubt, expert advice should be obtained. Naturally, for advisers, the Australian financial services licence under the CA and tax advice obligations under the Tax Agent Services Act 2009 (Cth) need to be appropriately managed to ensure advice is appropriately and legally provided.

DBA Lawyers offers a range of consulting services in relation to individuals and advisers who have queries about how an ‘ipso facto’ clause affects an SMSF. DBA Lawyers also offers a wide range of document services. DBA Lawyers also confirms that its LRBA documentation has been reviewed to ensure that it is up-to-date in light of the new law relating to ‘ipso facto’ clauses.

* * *

Note: DBA Lawyers hold SMSF CPD training at venues all around. For more details or to register, visit www.dbanetwork.com.au or call 03 9092 9400.

For more information regarding how DBA Lawyers can assist in your SMSF practice, visit

13 November 2018

Minimising lost opportunity: Payments above Account-Based Pension (‘ABP’) minimum

Joseph Cheung (jcheung@dbalawyers.com.au), Lawyer

and

Daniel Butler (dbutler@dbalawyers.com.au), Director, DBA Lawyers

Significant time has passed since the introduction of the transfer balance cap (‘TBC’). During this period, many have become aware of the potential trap caused by the TBC for SMSF members who receive payments above the account-based pension (‘ABP’) minimum annual amount, and have responded by implementing various strategies to avoid this trap. This article shows that timely action can minimise any further opportunity cost resulting from the trap.

What opportunity has been lost for those who have already been caught by the trap?

For members who have not implemented a strategy, the capital supporting their ABP(s) is reduced by the amount of the pension payment(s), including the amounts above the relevant ABP minimum(s). However, there is no corresponding debit to the member’s transfer balance account (‘TBA’)!

Where the member had ‘maxed out’ their TBC, they cannot add any further capital to commence a new pension that is in the retirement phase (ie, a pension that will obtain a pension exemption). Therefore, drawing more than the minimum payment will exhaust the capital supporting the ABP(s) significantly faster than would otherwise be the case. Where the member had not ‘maxed out’ their TBC, there will be limited capacity to add further capital to commence a new ABP.

EXAMPLE

As at 1 July 2017, Ken is 66 years old and has an existing ABP with $1.6 million capital supporting his ABP. He does not have any other pensions. He also has an accumulation superannuation interest of $100,000. On 1 July 2017, his personal TBC is $1.6 million. A credit of $1.6 million applies to Ken’s TBA.

On 1 August 2017, the SMSF trustee makes a payment of $200,000 to Ken. As Ken is 66 years old, the relevant ABP minimum payment for Ken is $80,000 (ie, $1,600,000 (account balance) x 5% (percentage factor)). Accordingly, this payment of $200,000 exceeds the ABP minimum payment for Ken by $120,000.

The result is that the capital supporting the pension is reduced by $200,000, with $1.4 million remaining (ignoring any growth and expenses). However, there is no corresponding debit to Ken’s TBA, which still shows a credit balance of $1.6 million. As Ken’s TBC is ‘maxed out’, he cannot add any capital to start a new pension.

If Ken does nothing and continues to receive pension payments greater than the relevant ABP minimum payment in this financial year (‘FY’) or in future FYs, the capital supporting the pension will be exhausted significantly faster than would otherwise be the case. Ken would not be able to add any capital to start a new pension.

How can members minimise lost opportunity?

DBA Lawyers understands that the following two-step strategy has been contemplated by many advisers in the SMSF industry to address the potential trap:

Step 1: Pay all amounts above the relevant ABP minimum(s) as a lump sum payment from the member’s accumulation interest.

Step 2: Where there is no accumulation superannuation interest or the accumulation superannuation interest is insufficient to pay the amounts in excess of the relevant ABP minimum(s), these excess amounts are to be paid as a partial commutation of the relevant ABP.

For members who already had an ABP on 1 July 2017, the effectiveness of the above strategy is maximised if it were documented on or shortly after 1 July 2017, so that the strategy applies prospectively before the payment of any amount above the relevant ABP minimum. In those circumstances, the members would have avoided the trap. For the avoidance of doubt, the strategy document should have been dated when executed. Note that backdating or falsification of a document is a serious matter that can result in substantial penalties.

As mentioned, some members may not have been aware or taken action. However, if the strategy is properly documented, these members can minimise any future lost opportunity.

EXAMPLE

This is a continuation of the earlier example. As at 1 July 2018, Ken is 67 years old and has an existing ABP with $1.4 million remaining. He does not have any other pensions. He also has an accumulation superannuation interest of $100,000. On 1 July 2018, Ken’s TBA still shows a credit balance of $1.6 million.

On 1 November 2018, the above two-step strategy is properly documented.

On 1 December 2018, the SMSF trustee makes a payment of $200,000 to Ken. As Ken is 67 years old, the relevant ABP minimum payment for Ken is $70,000 (ie, $1,400,000 (account balance) x 5% (percentage factor)). Accordingly, this payment of $200,000 exceeds the ABP minimum payment for Ken by $130,000.

As the strategy has been documented properly, the $70,000 is a payment from the capital supporting Ken’s pension, the $100,000 is a payment from Ken’s accumulation superannuation interest, and the $30,000 is a payment as a partial commutation of the ABP.

The result is that the capital supporting the pension is reduced by $70,000, with $1,330,000 remaining (ignoring any growth and expenses). Ken’s accumulation superannuation interest is fully exhausted, ie, reduced to nil. There is also a corresponding debit of $30,000 to Ken’s TBA, which now shows a credit balance of $1,570,000 (assuming no other events give rise to a debit/credit). As Ken’s TBC is not $1.6 million, he can add capital of up to $30,000 to start a new pension.

Alternatively, if no strategy had been documented, the result would be that the capital supporting the pension is reduced by $200,000, with $1.2 million remaining (ignoring any growth and expenses). However, there is no corresponding debit to Ken’s TBA, which still shows a credit balance of $1.6 million. As Ken’s TBC is ‘maxed out’, he cannot add any capital to start a new pension.

The above example shows that once the two-step strategy is documented, the capital supporting the pension will be exhausted slower than would otherwise be the case if the member had not put into place such a strategy. Even if a member had been caught in the trap, a result of documenting the strategy is that the lost opportunity resulting from the trap is limited to the period in which there is no strategy in place. Subsequent payments above the relevant ABP minimum(s) made in accordance with the strategy would not be exposed to the trap.

Can the strategy be documented to apply retrospectively?

Unfortunately, for members who have been caught in the trap, it is unlikely that the ATO would accept documentation that applies a strategy retrospectively, ie, after the payment of the amount above the relevant ABP minimum(s) has occurred.

In relation to the partial commutation of pensions, the ATO’s view, as expressed in TR 2013/5, is that the member must consciously exercise their right to exchange something less than their full entitlement to receive future pension payments for an entitlement to be paid a lump sum. Where no documentation exists either before or at the time of payment, it is hard to prove that the member consciously exercised their right. The ATO could decide that there was no partial commutation and that the amount was just paid as a pension payment in excess of the relevant ABP minimum(s). Accordingly, any strategy involving a partial commutation should be documented prior to the time of payment.

Similarly, where the payments are allocated and the strategy documented ‘after the fact’, the ATO might take the view that the payments did not come from an accumulation interest as it could not be proven that this was the parties’ intention at the time of payment, and it was not a valid partial commutation. The ATO could then treat the payment as a pension payment in excess of the relevant ABP minimum(s). A conservative approach is to have relevant documentation completed and signed before the payment of the amounts in excess of the ABP minimum payment.

Based on the above reasoning, members should take timely action to document a strategy so that the strategy can apply prospectively to the payment of any amount above the relevant ABP minimum.

Conclusion

SMSF members who have been caught in the trap caused by the TBC need to take timely action and prospectively record a strategy for payments above ABP minimums.

DBA Lawyers offers documentation to prospectively record the above strategy for any member who wishes to protect the capital supporting their pension(s) from being exhausted beyond the relevant minimum pension amount. For more information, please visit https://www.dbalawyers.com.au/payments-abp-minimum/.

* * *

Note: DBA Lawyers hold SMSF CPD training at venues all around. For more details or to register, visit www.dbanetwork.com.au or call 03 9092 9400.

For more information regarding how DBA Lawyers can assist in your SMSF practice, visit

15 October 2018

ALP’s franking credits policy targets shareholders with low taxable incomes

15 October 2018

Jim Bonham

“Having a non-means tested government payment solely on the criteria that you own shares and giving people a refund when you haven’t actually paid income tax for the year that the refund covers, what’s the economic theory behind that?” asked Opposition Leader Bill Shorten recently, and reported by Phillip Coorey in the Australian Financial Review on 12 October 2018.

Mr Shorten is talking about refundable franking credits, but actually franking credits are means tested (because they’re taxable income and our progressive tax scales are a form of means testing), and you have paid income tax (because franking credits are also pre-paid tax) and, finally, there is an economic theory (to ensure gross dividends are taxed as ordinary income).

Unfortunately, that’s not the way the ALP sees it.

Shadow Treasurer Chris Bowen, said refundable franking credits are “a concession”, “unfair revenue leakage” and “a generous tax loophole” when describing the ALP’s plan to stop the refunding of unused franking credits (see SuperGuide article https://www.superguide.com.au/smsfs/shorten-retirement-tax-refunds-franking-credits and and the ALP’s policy document, https://www.chrisbowen.net/issues/labors-dividend-imputation-policy/ )

Those comments are not right either. Refundable franking credits are part of an unfortunately convoluted and widely misunderstood process, but their function is straightforward: to ensure that Australian company profits distributed to Australian shareholders are taxed in the hands of the owners (shareholders) rather than the company, in exactly the same way as income from any other source. The company is only taxed on that part of its profit which is kept in the company for internal use, and not distributed.

In our present system of refundable franking credits therefore, there is no concession, no leakage and no loophole.

In the discussion referenced above, the Shadow Treasurer also said “While those people [with low taxable incomes] will no longer receive a tax refund, they will not be paying additional tax” which is a prime piece of Orwellian double-speak. It’s not correct, and shareholders on sufficiently low incomes will find that their franking credits are simply confiscated as tax – money they get now will no longer be received and they will have less to live on.

Australians on low incomes will lose franking credits, unless they receive a part or full Age Pension. After strong protests that convinced the ALP that its policy would actually harm those on low incomes, they announced the “Pensioner Guarantee” – an exemption from the policy for Age Pensioners who hold shares directly, and for SMSFs where at least one member received the Age Pension or a government allowance before 28 March 2018 – but that still doesn’t help non-pensioner shareholders with low incomes.

In this article, I dig into this subject in more detail, particularly for those who hold their shares directly in their own names, to show what the ALP proposal really means and how it would operate.

I’ll show that the policy can cause very substantial loss of income for direct shareholders, especially those on low or middle incomes. Retirees will simply not be able to suck up the sort of losses involved and we can expect some creative asset reduction to get under the Age Pension asset test threshold, or a major restructure of the investment portfolio to avoid franked dividends.

Dividend imputation, and how franking credits work

In the bad old days when dividends paid from company profits (taxable in Australia) were double-taxed, it worked like this: the company paid tax at the corporate rate (currently 30%) on the relevant profit; the remainder (70% at current rates) was sent as a dividend to the shareholders, who then paid further tax on it as part of their ordinary income.

In 1987, the Hawke-Keating government decided to remove this double taxation of dividends, introducing a dividend imputation system similar to what we have today, except that franking credits were non-refundable.

Although the company still paid tax at the corporate rate (currently 30%), any of that tax which was associated with profits paid out as a dividend was reclassified as a “franking credit” and held by the ATO as a pre-payment of tax on behalf of the taxpayer – very similar to the PAYE system

The franking credit was also treated as part of the shareholder’s taxable income. In other words, the gross dividend, which is the franking credit plus the dividend, was added to any other taxable income when calculating the shareholder’s income tax. The franking credits, being pre-paid tax, were then subtracted from the calculated tax owing, so that in the end the gross dividend was taxed just like any other income.

For high-income shareholders, whose tax liability exceeded the value of the franking credits, this system had the effect of transferring the liability for tax on company profits from the company to the shareholder.

However, for low-income shareholders the situation was different. If there were franking credits left over after paying the tax, the ATO simply kept the excess. (This outcome is what is meant by “non-refundable”). Taxpayers who would have paid no tax at all if the same amount had been earned from employment, actually paid the corporate tax rate on their dividends. Their dividend income was “taxed in their own hands”, but not taxed like other income.

In 2000, the Howard-Costello government made unused franking credits refundable to the taxpayer, creating the current system in which gross dividends are always taxed as shareholder’s income, regardless of the shareholder’s tax rate.

Here’s a simple example to show how the three systems treat low and high income taxpayers. For this example, “low income” means too low to pay tax in our current system and “high income” means over $180,000 so the marginal tax rate is 47% (including the Medicare levy). It’s also assumed that the gross dividend is not large enough to alter the taxpayer’s marginal tax rate, and today’s tax rates are used.

The table shows how much money, after tax, ends up in the shareholder’s pocket as a result of $100 profit earned by the company and distributed as a dividend. Clearly, low-income recipients of franked dividends will be the hardest hit if the ALP re-introduces non-refundable franking credits.

| System | After tax income from $100 profit | |

| Low income | High income | |

| Double taxation (prior to 1987) | $70 | $37 |

| Non-refundable franking credits (Hawke-Keating) | $70 | $53 |

| Refundable franking credits (Howard-Costello) | $100 | $53 |

Dividend imputation with non-refundable franking credits was a have-your-cake-and-eat-it-too system for the government, where that part of a company’s profits distributed as dividends was taxed at either the corporate or the personal tax rate, whichever gave the higher result. This is the system the ALP wants us to return to – Age Pensioners (mostly) excepted.

So who is most affected by the proposed policy? What is their income? How much income will they lose? How effective is the Pensioner Guarantee? Let’s look at these questions in some detail.

Significant loss of income under ALP proposal for direct shareholders

People who hold shares directly, outside of superannuation, may be rich or struggling; they may be retired or in their youth; they may rely on dividends from shares for all of their income, or just a part of it; they may have other taxable income from dividends, rental, employment etc. They might also receive non-taxable income from a superannuation pension, but that has to be looked at separately and does not affect what happens with their taxable income.

Whatever the circumstance, the introduction of the ALP’s policy will result in either a loss of income or, if the shareholder’s income is high enough, no change. No one gains except the government.

If a shareholder is going to lose income under the ALP policy, the actual amount depends on total taxable income, the amount of gross dividends as a percentage of the total, and whether the taxpayer is entitled to SAPTO (and if so, whether single or a member of a couple).

Incidentally, wherever I use the phrase “entitled to SAPTO”, it is to be understood that the entitlement only applies if the income is below the appropriate threshold. Above that, the “entitled to SAPTO” and “not entitled to SAPTO” curves in the graphs to follow are, of course, identical.

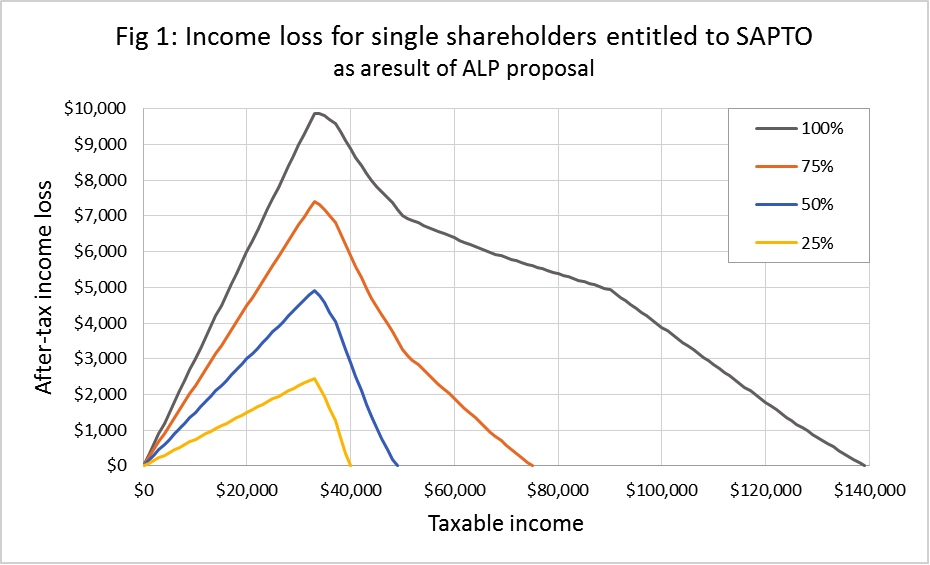

Fig 1 presents the loss of income which would result from the ALP proposal for a single senior shareholder entitled to SAPTO, where the gross dividends received constitute 25%, 50%, 75% or 100% of the shareholder’s total taxable income.

For example, if gross dividends represent 100% of a taxpayer’s income, the introduction of the ALP proposal will be most financially devastating for single senior Australians earning about $33,000 a year but will also affect those earning up to about $138,000 a year. If gross dividends represent 75% of a taxpayer’s income, the ALP proposal will most severely hurt single senior Australians earning about $33,000 a year but will also affect those earning up to about $75,000 a year

In all scenarios, single senior Australians with low to moderate incomes will be most affected by the ALP’s proposal to ban franking credits refunds.

Figure 2 shows the same results, but for a senior taxpayer who is a member of a couple. Note this graph is just one partner’s share of both the income and the loss. The shapes of the curves are a bit different from those in Fig 1 because of the complicated structure of our tax scales.

Note: In particular, for a couple, if gross dividends make up 50% or less of total income, the worst loss occurs at an income (each) of about $22,000.

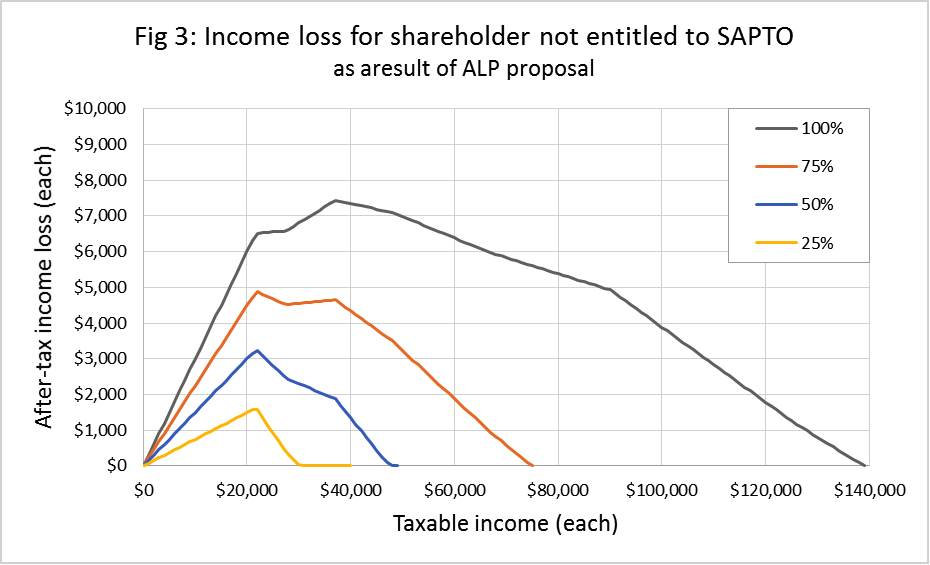

Finally, Fig 3 shows the same results for a younger taxpayer who is not entitled to SAPTO.

In each of these three graphs the curves are skewed towards lower incomes and the greatest amount of income loss occurs at a taxable income of between $22,000 and $33,000 depending on the individual case. That’s hardly a huge income, yet in the worst case the ALP proposal will reduce this income by up to $10,000 per year, depending on the percentage of franked shares contributing to taxable income. The proportional loss is savage.

For those who don’t qualify for SAPTO, the maximum loss of income occurs at lower taxable incomes and is not quite as large, but it is still very significant in relation to the level of income

This is just another slap in the face to seniors who, in recent years, have suffered the doubling of the Age Pension asset test taper rate, dramatic upheaval in the structure of superannuation in retirement and now, for share investors, the threat of losing some or all of their franking credits.

Many retirees must question why they put so much effort in their younger years into saving and learning how to invest, only to have their assets and income so badly trashed by continually changing rules.

What about the Age Pension?

When introducing this policy, the ALP claimed that it would mostly affect wealthy retirees. A strong backlash led to the Pensioner Guarantee (exemption) and the claim that they were thus protecting those less well off.

However, that did nothing for those who fail to qualify for the Age Pension but still don’t have much income. We need to see where in Figs 1 or 2 the Age Pension might cut out.

To keep things as simple as possible, we’ll just look at the top curves in Figs 1 and 2, which assume that gross dividends make up all the taxable income. In both cases, the worst loss occurs for a taxable income of about $33,000, and if we assume a gross dividend yield of 6% (approximately the average for fully franked shares in the ASX 200) the value of the shares needed to generate that income is $550,000.

The upper asset test threshold for the Age Pension is different for singles and couples, and for those who own their own homes:

| Asset test upper threshold | ||

| Homeowner | Not homeowner | |

| Single | $564,000 | $771,000 |

| Couple (each) | $424,000 | $511,000 |

None of these figures are very far from $550,000. What that means is that someone who just fails to qualify for the Age Pension, and so is not excluded from the ALP policy, will probably find themselves facing close to the maximum loss of income.

How will people respond?

With incomes at these levels, nobody’s going to just suck up the sort of losses involved, so expect either (a) some creative asset reduction to get under the Age Pension asset test threshold, or (b) a major restructure of the investment portfolio to avoid franked dividends.

The first alternative, that is, creative asset reduction, is likely to trap the person into permanent dependence on the Age Pension, restricting a person’s ability to improve her financial position in future or to deal with major health or care issues late in life. The second alternative, restructuring the investment portfolio, could adversely affect the risk of the portfolio producing poor returns, leading to an inadvertent slide onto the Age Pension.

Either way the objective of the ALP proposal is thwarted, which makes it rather pointless to make people jump through these hoops, while putting more people on the Age Pension

SMSFs also hit by ALP proposal

The ALP’s proposal also applies to shares held within a self-managed super fund.

If an SMSF is in accumulation mode, then the tax rate on investment earnings and discounted capital gains is 15%. In such circumstances, if gross dividends make up more than half the total income, some of the franking credits will be lost. I suspect most people caught in this situation will restructure their investments to bring gross dividends down below 50% of income. Such a strategy solves the tax problem, but may adversely alter the SMSF’s risk profile.

SMSFs in pension mode are in a much more difficult situation. They pay zero tax on fund earnings, but under the ALP proposal they would lose all of their franking credits, which could be up to 30% of their current income. Portfolio restructure is one option to avoid this tax (although it would mean abandoning shares paying franked dividends), as is simply reducing (spending) assets so as to bring their value low enough to qualify for the Age Pension – in both cases with the possible consequences outlined earlier.

Unfortunately, reducing the value of shares held in the SMSF – as a deliberate strategy or simply to supplement income – to the point where a retiree qualifies for a part Age Pension still won’t protect the franking credits. The Pensioner Guarantee does not apply to SMSF members who qualify after 28 March 2018, so retirees in this situation will probably consider closing their SMSF and reinvesting outside super.

SMSFs in pension mode seem to be the main target of the ALP’s proposal, and the Shadow Treasurer’s statement (https://www.chrisbowen.net/issues/labors-dividend-imputation-policy/ ) specifically refers to the fact that some SMSFs get very large refunds of franking credits. Well yes, some did, but that was largely eliminated by capping superannuation pension accounts at $1.6 million. Meanwhile, lots of people have relatively small SMSF pension accounts.

If the real problem that the ALP is trying to address is the fact that SMSFs in pension mode pay no tax, then that should be addressed directly with full consideration of context including large funds as well as SMSFs. It is a fundamental and complex issue and simply changing the way dividends are taxed is not the way to deal with it.

Destructive and unfair tax policy

Halting the refund of excess franking credits is a very destructive policy for those who hold shares directly or in an SMSF, especially in pension phase

Such a proposal puts a severe strain on retirees whose taxable income is fairly low unless they can find a way to restructure their investments or qualify for the Age Pension, but it has little or no effect on wealthier people – unless their investment is through an SMSF in pension mode.

Likely responses to the policy would see some people driven to the Age Pension, at long-term cost to themselves and the government. Others will close their SMSF purely to get under the umbrella of the Pensioner Guarantee. Some may decide to remove all Australian shares paying franked dividends from their portfolios – how is this good for themselves or the country?

Income tax is often arbitrary and complex, but the basic principle of dividend imputation with refundable franking credits is simple and sound: to ensure profits distributed as dividends are taxed as normal income in the hands of shareholders. Why mess that up?

The ALP policy is the antithesis of a well-designed tax policy, a direct slap in the face to the notion of a progressive tax system, and an extraordinary proposition to have come from the ALP.

Exempting Age Pensioners who hold shares directly from this policy was painted as supporting those on low incomes, but really it was just a way of papering over part of a problem and hoping no-one would notice the rest.

Technical note: All tax calculations in this article use 2018-19 tax rates, and include LITO, LMITO, SAPTO (if relevant) and the Medicare levy. The Age Pension asset test thresholds are applicable from September 2018. For more information on income tax rates see SuperGuide article https://www.superguide.com.au/boost-your-superannuation/income-tax-rates. For more information on Age Pension assets test, see SuperGuide article https://www.superguide.com.au/accessing-superannuation/age-pension-asset-test-thresholds .

About the author: Jim Bonham

Dr Jim Bonham is a retired scientist and R&D manager, who is deeply concerned about the appalling instability of the regulatory environment around superannuation, retirement funding and investment generally. If the ALP policy is implemented, he will be affected by the loss of franking credits in relation to shares held directly, and within an SMSF.

Copyright: Jim Bonham owns the copyright to this article. Copyright © Jim Bonham 2018

First published on 15 October 2018 on SuperGuide: https://www.superguide.com.au/retirement-planning/alps-franking-credits-policy-targets-shareholders-low-taxable-incomes

On 16 October 2018 Jim Bonham sent the following email to Bill Shorten and Chris Bowen:

From: Jim Bonham [mailto:jim@bonham.id.au]

Sent: Tuesday, 16 October 2018 9:19 AM

To: ‘Bill.Shorten.MP@aph.gov.au‘ <Bill.Shorten.MP@aph.gov.au>

Cc: ‘Chris.Bowen.MP@aph.gov.au‘ <Chris.Bowen.MP@aph.gov.au>

Subject: Franking credits

Dear Mr Shorten,

I was dismayed to read the following quote, attributed to you, regarding refundable franking credits:

“Having a non-means tested government payment solely on the criteria that you own shares and giving people a refund when you haven’t actually paid income tax for the year that the refund covers, what’s the economic theory behind that?” (https://www.afr.com/news/bill-shorten-promises-biggest-preelection-policy-agenda-since-gough-whitlam-20181011-h16ju0 )

The facts are:

- Refunds of franking credits to shareholders with low taxable income are means tested, because franking credits are taxable income and the progressive nature of income tax system effectively applies a means test.

- You have paid income tax, because the franking credit is treated by the ATO as a pre-payment of tax. The refund to those on low taxable incomes occurs because the pre-payment is an over-payment.

- There is an economic theory. The dividend imputation process was designed to ensure that company profits distributed as dividends are taxed in the hands of the shareholder (the company is only taxed on profits retained for internal use). Refunding franking credits in excess of the shareholder’s tax obligation is essential to ensure that the gross dividend is taxed in the same way as other income. Failing to refund excess franking credits, as the ALP is proposing, forces those on low taxable incomes to pay a higher rate of tax on gross dividends than they would if the same income were earned in any other way.

Please abandon the policy of making franking credits non-refundable. It hits those with low taxable incomes the hardest, and makes living in retirement on your own resources far more difficult for self-funded retirees.

Jim Bonham

How did both major parties get super so wrong?

The Australian

1 October 2018

Robert Gottliebsen – Business Columnist

Both the government and the opposition have the same problem — they both have difficulty in devising sensible superannuation and retirement policies.

And this raises the question of why can’t they get it right? Why do they make so many mistakes?

In the Weekend Australian I set out how shadow treasurer Chris Bowen simply got his franking credits policy wrong.

But go back a few years and the then treasurer Scott Morrison and his assistant Kelly O’Dwyer put forward a set of horrendous superannuation policies and even went as far as saying they were not retrospective when of course everyone knew they were.

Those bad policies almost cost the Coalition the election. They were lucky because many of their backbenchers took the trouble to talk to people and understand what was happening and forced through policy adjustments that were at least a substantial improvement on the original ideas.

And in the current ALP fiasco my understanding is that, in a similar way to the Coalition, intelligent backbenchers are talking to the voters and are starting to understand the looming disaster and are desperately looking for a way around the problem without admitting error.

Let me help them. The best way is to abandon the policy altogether, but if you need a compromise then limit the amount of cash franking credits that can be claimed to, say, about $15,000.

The cap being floated in ALP circles is $10,000 but I think that is too low. But whether it be $10,000 or $15,000, the problem is we are introducing legislation that is complex, will raise very little money and makes retirement just that much more complex.

We can fix that over time, and a $15,000 annual cap to cash franking credits will solve most of the problems among the battlers who are struggling to fund their own retirement. The problem both the Coalition and the ALP face in superannuation matters is that, in the first instance, the politicians have very generous super arrangements and don’t do their homework on the rest of the population. Even worse, in the public service the people at the top are mostly on incredibly generous benefits and are members of the so-called “$10 million club” with benefits that are way in excess of what is available to the general public.

While that has been changed for the most recent recruits, the people at the top of the public service are mostly living in a different world to the rest of the country. So when they look at super and retirement matters they simply have no idea what is taking place. My understanding is Chris Bowen, when devising his super franking credit disaster, actually went to the public service to have it evaluated and they came back with the thumbs up, which made him confident that the concept was a legitimate tax arrangement that would take money from the rich.

As we all now know, the policy is a savage blow to ordinary Australians trying to fund retirement, with about 1.4 million people in the ALP’s sights and hardly a rich person among them.

I believe we are looking at a phenomenon that cripples both parties. The first step in solving the problem is that ministers in areas like superannuation need to understand that the public service is of limited value to them.

They have to send their people out into the real world and, as the Coalition found, the best advice came from the backbenchers who usually have the time to be in touch with the electorate.

Ministers and shadow ministers in Canberra (and also in state governments) surround themselves with ministerial staff who second-guess the public service. Too often the ministerial staff are “yes” people with no depth to their knowledge outside of politics.

This situation has caused many talented people to either leave the public service or simply not join it. Once we had a proud public service that was as far as possible independent, but we are now seeing in so many areas public service advice simply doesn’t have the same standards it once did.

Nothing is going to happen in the short term, but down the track ministers are going to have to think about how they restore the quality of public service advice so that they don’t get caught in situations as we have seen in superannuation and retirement from both parties. When Australians reach their 40 and 50s they make long-term plans for their retirement in accordance with rules that exist at the time. When past governments changed rules the old rules were grandfathered so they were not retrospective.

It was the Coalition that decided there should be retrospective legislation. At least Bowen is being honest and is saying he is changing the rules retrospectively, but that doesn’t validate his policy. For what it is worth I admire the shadow treasurer for the fact that he is open about the tax measures he is planning to undertake.

Traditionally opposition treasurers keep their mouths shut and introduce the nasties once they get into office.

For real Scomentum, drain the billabong

The Spectator

26 September 2018

David Flint

Our political class are being seen more and more as arrogant and as out of touch as the French aristocracy were in the lead-up to the revolution.

The people who decide elections— those who are not rusted-on Coalition or Labor voters— see little difference between them. Most have neither the time nor the interest to go into the detail which would demonstrate that, however inadequate government policy is, Labor’s is worse. And the only news most see is on TV bulletins where someone from the gallery typically presents politics through a left-wing prism

Seeing little difference in policy, the undecided see only one thing, disgraceful self -indulgence, the latest being for many the last straw. They will make the government pay, however much Labor is involved.

Before I discuss that, the crucial thing in any poll, at least in Australia, is the ‘two-party preferred vote’ the two-party preferred. Everything else is décor.

The latest, 44/56, demonstrates that Scott Morrison has to show his policies are significantly different and what the people want. He has at least acted to retain the Catholic vote which Simon Birmingham lost, a vote Menzies long ago seduced from Labor by acting on the grossly inequitable treatment of the parochial school system.

Following the constitution, Canberra should otherwise keep its nose out of schools, as should all politicians. Using schoolchildren as political props does not attract votes. In fact, most voters are sickened by this form of child abuse.

To win, Scott Morrison must adopt policies significantly different from Labor’s on energy, the rate of immigration and pouring taxpayers hard-earned money down the drain. He should spend a few hours with Tony Abbott who’ll put him right.

He should also announce a plan to drought-proof the country, with Stage 1 to be completed in five years. This should incorporate the three B’s —the Bradfield, Beale and Bridge Plans. He can borrow this from Alan Jones who’ll be delivering a major address on this next week, see www.norepublic.com.au

Morrison should also apologise to the Liberal base who’ve walked out or gone on strike by repealing the dopey superannuation legislation he and Kelly O’Dwyer pushed through. Not only does this offend just about everything the Liberal Party stands for, it has encouraged Labor not only to do worse but to announce it knowing that the Liberals can’t complain — some achievement.

He must also appoint a real and not a jack-in-the-box Minister of Defence, one whom the military would respect. Morale is at an all-time low from the Canberra-assisted campaign against war heroes, the way cultural Marxists are running recruitment and the raids on the defence budget, bigger even than Labor’s, to shore up government seats.

The last straw for many undecided was the award to two politicians of travel so luxurious as to be beyond the wildest dreams of most Australians. This involves a three-month stay in luxury accommodation in New York at a cost of about $100,000 each. Neither the Liberal, Anne Sudmalis, nor Labor’s Jenny Macklin, can make the usual feeble argument that this will enable them to better represent their constituents by improving their understanding of the UN, global government and how and why our sovereignty is being sold out to the rule of international bureaucrats from an organisation dominated by foreign dictatorships.

Almost as soon as they return, both will take their parliamentary superannuation, possibly picking up ‘jobs for the boys’ and well-paid postings in foreign corporations, banks and other places.

While some will recall Ms Macklin’s role as a great distributor of taxpayer-funded largesse, Ms Sudmalis only rose to prominence with her recent unpersuasive complaints about ‘bullying’ within the Liberal Party. Her face, but not her name, was however well-known by being placed strategically behind the PM during Question Time, that fourth-rate version of the real question time at Westminster where the Speaker chooses the questioners. Her involvement in this farce may not have raised her prestige, her job being either to nod approval to whatever ministers read from their prepared answers or to laugh at their attacks on the opposition.

As a result of ‘bullying’ and not because the seat will be among the first to fall in the election, Ms Sudmalis announced she will seek re-election.

Since neither indulgence involves Bronwyn Bishop, the mainstream media has not continued to pursue them. Nevertheless, in workplaces, kitchens, clubs and pubs across the country and in people’s memory, this rort is a subject of outrage where the common lament is that this time the politicians have gone too far.

Marie-Antoinette, who never even saw the sea, was guillotined for less. In fact, she never said of the starving poor “Let them eat cake”. That was an invention of the fake media of the day. In fact, all of the charges against her were concocted by the Jacobins, as if they were Democrats undermining a Republican judicial nomination in Washington.

Meanwhile, in Australia, the parties and their leaders do not seem to realise how this grotesque indulgence is a slap-in-the-face for the farmers who are persecuted constantly by the politicians and bureaucrats who have stolen their water and turned vast parts of their land into carbon sinks to venerate the fashionable and foreign religion of global warming.

Nor do they see how this excess has so outraged those hard-working taxpayers who are paying not only for the politicians but for the armies of apparatchik-advisors wholly unknown at the time of Menzies and Fraser, the vast numbers of bureaucrats now paid at imagined private sector rates, the brigades of consultants and now, an emerging class of crony capitalists created by substituting political patronage for the essence of the free enterprise system, risk.

Thus an increasingly vast part of the economy, supposedly free enterprise, is simulating that of the banana republic Mr Shorten wishes to force onto a reluctant nation.

This once again presages a descent into, if not the Venezuela, the Argentina of the South Seas. This can only be reversed by fundamental reforms to the governance of this country.

The 2016-2017 adverse superannuation changes; a Grattan Institute/Turnbull Government recipe for loss of trust and increased uncertainty?

Address by Jack Hammond QC, founder of Save Our Super.

Tuesday, 18 September 2018 at La Trobe University Law School, City Campus, 360 Collins Street, Melbourne, lunch-time seminar, “Australian Superannuation: Fixing the Problems”.

INTRODUCTION and DECLARATION OF INTEREST

In 2016-17, the Turnbull Government made a number of superannuation policy and legislative changes which adversely affected many Australians. Those changes were made without appropriate ‘grandfathering’ provisions even though they amounted to ‘effective retrospectivity’ (a term coined in February 2016 by the then Treasurer, Scott Morrison). ‘Grandfathering’ provisions continue to apply an old rule to certain existing situations, while a new rule will apply to all future cases.

I am a retired barrister and am adversely affected by those 2016-17 superannuation changes. That, in turn, has led me to form the superannuation community action group, Save Our Super.

The Turnbull Government, assisted and encouraged by the Grattan Institute in Melbourne has, without notice and at a single stroke, changed the superannuation rules and the rules for making those rules. They have turned superannuation from a long-term, multi-decades, retirement income system into, at best, an annual federal budget-to-budget saving proposition. That is a contradiction in terms . It is unsustainable.

Further, it is a recipe for a loss of trust and increased uncertainty for all those already in the superannuation system and those yet to start.

Save Our Super has three proposals which we believe will redress the 2016-17 superannuation policy and legislative changes and prevent a recurrence.

But first, how did we get here and in particular, without appropriate ‘grandfathering ‘ provisions? Those type of provisions have accompanied all significant adverse superannuation changes over the past 40 years.1

BACKGROUND CHRONOLOGY

| 29 November 2012 | Lucy Turnbull appointed a director of the Grattan Institute, Melbourne.2 |

| May to June 2015 | Scott Morrison, whilst Minister for Social Services in Abbott Government, makes 12 ‘tax-free superannuation’ promises.3 |

| 2014 to 2015 | Malcolm and Lucy Turnbull donate funds to Grattan Institute.4 |

| 15 September 2015 | Malcolm Turnbull replaced Abbott as Prime Minister. Scott Morrison becomes Treasurer.5 |

| 24 November 2015 | Grattan Institute publishes Report ”Super Tax Targeting” by Grattan Institute CEO John Daley and others. Dismisses need for ‘grandfathering’ provisions6 and observes ‘…that taxing earnings for those in the benefits stage may raise concerns about the government retrospectively changing the rules’. 7

No mention of the possible consequential of loss of trust and uncertainty that retrospective changes may bring. Note that the Grattan Institute material shows, on its front page, an image of three of the bronze pigs on display in the Rundle Street Mall, Adelaide.8 We, and other self-funded superannuants, believe that the Grattan Institute’s prominent use of that image of those bronze pigs was not merely a juvenile attempt at humour. It was a none-to-subtle insulting implication that Australians whom had faithfully conformed with successive governments’ superannuation rules and had substantial superannuation savings were, nonetheless, greedy pigs with their ‘snouts in the trough’. See also 9 November 2016 entry below. |

| 2015-2016 | Malcolm and Lucy Turnbull donate further funds to Grattan Institute.9 |

| 18 February 2016 | Scott Morrison, as Treasurer, gave an address to the Self Managed Superannuation Funds 2016 National Conference in Adelaide.

Draws attention to ‘effective retrospectivity’ and its ‘great risk’ in relation to super changes. “Our opponents stated policy is to tax superannuation earnings in the retirement phase. I just want to make a reference less about our opponents on this I suppose but more to highlight the Government’s own view, about our great sensitivity to changing arrangements in the retirement phase. One of our key drivers when contemplating potential superannuation reforms is stability and certainty, especially in the retirement phase. That is good for people who are looking 30 years down the track and saying is superannuation a good idea for me? If they are going to change the rules at the other end when you are going to be living off it then it is understandable that they might get spooked out of that as an appropriate channel for their investment. That is why I fear that the approach of taxing in that retirement phase penalises Australians who have put money into superannuation under the current rules – under the deal that they thought was there. It may not be technical retrospectivity but it certainly feels that way. It is effective retrospectivity, the tax technicians and superannuation tax technicians may say differently. But when you just look at it that is the great risk.”10 |

| 3 May 2016 | Scott Morrison, as Treasurer, announces in his Budget 2016-17 Speech to Parliament a number of adverse ‘changes to better target superannuation tax concessions’ .

No ‘grandfathering’ provisions announced.11 See also, Budget Measures, Budget Paper No 2, 2016-17, 3 May 2016, Part 1, Revenue Measures, pp 24-30.12 |

| 5 September 2016 | John Daley, CEO Grattan Institute, said: “Winding back superannuation tax breaks will be an acid test of our political system. If we cannot get reform in this situation, then there is little hope for either budget repair or economic reform” (AFR 5/9/16)13 |

| 9 November 2016 | To give effect to the Budget 2016-17 superannuation changes, Scott Morrison presented the Turnbull Government’s package of 3 superannuation Bills to Parliament.

To publicly explain and justify those superannuation changes to Parliament, Scott Morrison and Kelly O’Dwyer circulated and relied in Parliament upon a 364 page “Explanatory Memorandum”. The Explanatory Memorandum states on its front page “Circulated by the authority of the Treasurer, the Hon Scott Morrison MP and Minister for Revenue and Financial Services, the Hon Kelly O’Dwyer MP.” In turn, the Explanatory Memorandum expressly refers to, and provides links to, the Grattan Institute’s 24 November 2015 Media Release and Report (see 24 November 2015 entry, above). As noted above, that Grattan Institute material shows, on its cover, an image of three of the bronze pigs on display in the Rundle Street Mall, Adelaide.14  Bronze pigs in Rundle Street Mall, Adelaide |

| 23 November 2016 | The Turnbull Government, with the support of Labor, rushed through Parliament two of its three superannuation Bills. |

| 29 November 2016 | Those two Bills were assented to on 29 November 2016 and are now law:

Superannuation ( Excess Transfer Balance Tax) Imposition Act 2016 (C’th) (No 80 of 2016);15 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act 2016 ) (C’th) (No 81 of 2016)16 The third superannuation Bill, the Superannuation (Objective) Bill, remains stalled in the Senate.17 |

| 1 December 2016 | Lucy Turnbull retired as a director of the Grattan Institute.18 |

| 24 August 2018 | Malcolm Turnbull resigns as Prime Minister.19 Scott Morrison becomes Prime Minister.20 |

SAVE OUR SUPER’S THREE PROPOSALS FOR THE FUTURE

Save Our Super has three proposals which we believe could redress the 2016-17 superannuation policy and legislative changes and prevent a recurrence.

First, Scott Morrison, in his new capacity as Prime Minister, should request the Treasurer, Josh Frydenberg and/or through him, the Assistant Treasurer, Stuart Robert, to revisit the Turnbull Government’s 2016-17 superannuation changes.

A discussion paper and advice from Treasury should be requested. It should include the effect of the Turnbull Government’s 2016-17 superannuation changes on superannuation fund taxes in 2017-18 and over the forward estimates.

To restore trust and reduce uncertainty in the superannuation system, the Morrison Government should introduce into Parliament legislation which will retrospectively provide appropriate ‘grandfathering’ provisions in relation to the Turnbull Government’s 2016-17 adverse superannuation changes.

Those ‘grandfathering’ provisions to be available to those significantly adversely affected and whom wish to claim that relief.

Secondly, Save Our Super proposes to create a Superannuation and Retirement Income Policy Institute, independent of government , funded, at least initially, by private donations/subscriptions.

Its role will be to advocate on behalf of those millions of superannuants and retirees whose collective voice needs to be heard.

Thirdly, Save Our Super will advocate for an amendment to the Australian Constitution, to have a similar effect in relation to superannuation and other retirement income, as does section 51 (xxxi) has in relation to the compulsory acquisition of property.

That section empowers the federal Parliament to make laws with respect to the acquisition of property on just terms from any State or person for any purpose in respect of which the Parliament has power to make laws (emphasis added).

Thus Parliament’s power to make laws in relation to superannuation and other retirement income should not be affected. However, any significant adverse change to existing situations will need to be on just terms, for example, by providing appropriate ‘grandfathering’ provisions as part of that federal law.

1. [https://saveoursuper.org.au/super-changes-grandfathering-rules-must-considered]↩

2. [https://grattan.edu.au/wp-content/uploads/2014/03/Grattan_Institute_Annual_Financial_Report_2013.pdf (pp 2-3)]↩

3. [https://saveoursuper.org.au/scott-morrison-12-superannuation-tax-free-promises]↩

4. [https://grattan.edu.au/wp-content/uploads/2015/11/Grattan-Institute-Annual-Report-on-Operations-30-June-2015.pdf (p 19)]↩

5. [https://en.wikipedia.org/wiki/First_Turnbull_Ministry]↩

6. [https://grattan.edu.au/wp-content/uploads/2015/11/832-Super-tax-targeting.pdf (p 7)]↩

7. [https://grattan.edu.au/wp-content/uploads/2015/11/832-Super-tax-targeting.pdf (pp 68-9, para 6.5)]↩

8. [https://grattan.edu.au/wp-content/uploads/2015/11/832-Super-tax-targeting.pdf (front page)]↩

9. [https://grattan.edu.au/wp-content/uploads/2016/11/Grattan-Institute-Annual-Report-on-Operations-30-June-2016.pdf (p 24)]↩

10. [Scott Morrison, Address to the SMSF 2016 National Conference, Adelaide]↩

11. [https://www.budget.gov.au/2016-17/content/speech/html/speech.htm]↩

12. [https://budget.gov.au/2016-17/content/bp2/download/BP2_consolidated.pdf]↩

13. [https://grattan.edu.au/wp-content/uploads/2017/11/Grattan-Institute-Annual-Report-2017-Web.pdf (p 6)]↩

14. [The Explanatory Memorandum refers to the Grattan Institute’s 24 November 2015 report “Super tax targeting” by John Daley and Brendan Coates: (see page 275, paragraph 14.12, footnote 2). Click on the link on footnote 2, “2 Grattan Institute, media release, ‘For fairness and a stronger Budget, it is time to target super tax breaks’, 24 November 2015, http://grattan.edu.au/for-fairness-and-a-stronger-budget-it-is-time-to-target-super-tax-breaks/”.

Click on the link at foot of that page “Read the report“. That link will take you to the Grattan Institute report “Super tax targeting “ dated 24 November 2015 by John Daley and others. The report’s front page shows the image of those bronze pigs in the Rundle Street Mall, Adelaide. Note: The Grattan Institute’s website has been updated since the publication of that document. However, the article itself and the image of the 3 pigs remain.]↩

15. [Superannuation ( Excess Transfer Balance Tax) Imposition Act 2016 (C’th) (No 80 of 2016)]↩

16. [Treasury Laws Amendment (Fair and Sustainable Superannuation) Act 2016 ) (C’th) (No 81 of 2016)]↩

17. [Superannuation (Objective) Bill]↩

18. [https://grattan.edu.au/wp-content/uploads/2017/11/Grattan-Institute-Annual-Financial-Report-2017.pdf (p 3)]↩

19. [https://en.wikipedia.org/wiki/Malcolm_Turnbull]↩

20. [https://en.wikipedia.org/wiki/Scott_Morrison]↩

Australian Superannuation: Fixing the Problems – Free lunch-time seminar at La Trobe University Law School – Melbourne City Campus – 18 September 2018

On Tuesday, 18 September 2018, La Trobe University Law School, in conjunction with Save Our Super, will present a free lunch-time seminar, Australian Superannuation: Fixing the Problems.

It will be held at La Trobe University’s Melbourne City Campus at 360 Collins Street, Melbourne.

Key speakers will be Professor Nicholas Morris, author of Management and Regulation of Pension Schemes: Australia – A Cautionary Tale, and Jack Hammond QC, the founder of Save Our Super, the superannuation community action group.

Below is an abstract of the seminar subject-matter.

If you wish to attend this lunch-time seminar, please click on the following link and register. Places are limited, so please register early:

https://www.eventbrite.com/e/australian-superannuation-fixing-the-problems-tickets-49460527770

Abstract:

In the past few weeks, the Hayne Royal Commission has exposed numerous problems with the Australian superannuation system. These include alleged: “unconscionable conduct over the charging of fees”; ineffective regulatory action by both APRA and ASIC; failures of trustees to “prioritis[e] the interests of members over the interests of themselves and related parties”; and numerous alleged breaches of both the Corporations Act and the Superannuation Industry (Supervision) Act. The evidence heard by the Royal Commission reinforce those of the Productivity Commission, published in May this year, and of Professor Nicholas Morris, whose book Management and Regulation of Pension Schemes: Australia – A Cautionary Tale was published in April 2018.

This seminar follows a previous La Trobe Law School seminar, “Australian Superannuation: What went wrong?”, held on 1 August 2018.

In this seminar, Professor Morris will be joined by Jack Hammond QC, the founder of superannuation community action group Save Our Super to discuss what can be done to improve the situation. Their wide-ranging suggestions will draw both on those set out in Professor Morris’ book and those identified through interaction with Save Our Super supporters. They will include reforms to regulatory and legal arrangements, increased transparency, and the introduction of a more accountable fund against which the performance of other funds can be benchmarked. Professor Louis de Koker will then chair a discussion among seminar participants.

Presenters

Professor Nicholas Morris is an adjunct professor at La Trobe School of Law. He is the author of Management and Regulation of Pension Schemes: Australia – A Cautionary Tale (Routledge, 2018) and co-editor of Capital Failure: Rebuilding Trust in Financial Services (Oxford University Press 2014, paperback 2016). He has advised governments, industry and regulators on regulatory and investment issues, worldwide, for over 40 years.

Jack Hammond QC is the founder of superannuation community action group Save Our Super. He was a Victorian barrister for more than three decades. Prior to becoming a barrister, he was an Adviser to Prime Minister Malcolm Fraser.

* * * * * * * * * * * *

Response to Treasury Discussion Paper: Three-yearly audit cycle for some self-managed superannuation funds

Copyright © Jim Bonham 2018

1 Summary

As an SMSF trustee, I am concerned about the proposal to introduce three-year audits for some SMSFs, primarily for the following reasons:

- None of the three benefits claimed for the proposal (reduction of compliance burden, reduction in audit cost, and rewarding the timely submission of SARs) withstands examination.

- Audit management will become more complex for the trustee, increasing the risk of inadvertent rule breaches.

I would not opt for a three year audit of my SMSF if this proposal becomes law.

2 Introduction

My wife and I have an SMSF under a corporate trustee structure. The fund was started in 2003 and has been totally in pension mode for several years. The SMSF and some investments outside superannuation will be our only sources of income for the rest of our lives, and this does tend to focus the mind.

Each year, we provide the fund’s financial and share-trading data to our accountant who prepares the tax return etc, sends us a draft for checking and then forwards everything to the auditor. Following satisfactory audit (we have never had a problem), the SAR is then forwarded to the ATO without further intervention by us.

Given the complexity and instability of superannuation rules, we feel the multiple checkpoints in this process provide good protection against unintentional infringements which could see us in trouble with the ATO – a potentially costly and stressful outcome we are very keen to avoid. They can also help protect us against unwittingly increasing our investment risks.

The proposal to introduce an optional three year audit cycle for some SMSFs (which would include our fund) is therefore of considerable concern to us. We see heightened risk with no material compensatory benefit. Given the choice, we would not opt for three-yearly audits.

Below I provide more detailed comments in response to the specific Consultation Questions raised in the Discussion Paper

On 26 July, I had the opportunity to participate in a Treasury round-table discussion about this proposal, which I appreciated very much. I was there to present a trustee’s view point, not that of any organisation, and I made some of the following comments at that meeting.

3 Consultation questions

3.1 How are audit costs and fees expected to change for SMSF trustees that move to three-year cycles?

This is a critical question, there being no point going ahead with the proposal if costs are to rise, so I would like to discuss it in detail with reference to each of the three benefits claimed and the two concerns mentioned on Page 3 of the Discussion Paper.

3.1.1 Benefit 1: “A reduction in the compliance burden …”

I cannot see the basis for this claim, given the following comments from other parts of the discussion paper:

- “It is proposed that eligibility … will be based on self-assessment” (Page 4)

- “If the ATO becomes aware that a SMSF trustee has incorrectly assessed their eligibility for a three-yearly audit cycle, … the ATO will notify the trustee that an audit is required and consider further action if necessary” (Page 4)

- “ .. a number of events can represent a material change to the situation of the fund and may increase the risk of a breach …” (Page 5)

- “If a key event falls in a year when an SMSF is not otherwise to be audited, the SMSF will be required to obtain an audit … required to cover all financial years since the SMSF’s last audit” (Page 5)

- Eight “possible key events” are listed on Page 5, with a request for suggestions.

It is crystal clear that moving some SMSFs to a three-year audit cycle will create a more complex compliance landscape.

This must increase the risk of inadvertent breaches. Trustees who opt for three-yearly audits will have to become aware of a greater number of rules, and be vigilant that they do not inadvertently fail to report a key event.

Both these aspects of three-year audits increase the compliance burden, rather than decreasing it.

In addition, the appalling instability of superannuation legislation suggests there is a very high likelihood that, if three-year audits are introduced, the list of key events will change and be extended over time – further exacerbating compliance worry and risk.

It is unlikely that the trustee or accountant will be spared any administrative effort by moving to a three-year audit cycle, because exactly the same set of transactions will eventually have to be presented for audit as with annual audits.

The second part of the first claimed benefit “… while maintaining appropriate visibility of errors in financial statements and regulatory breaches” just does not make sense. How can visibility be maintained if a transaction is not audited for two or three years?

3.1.2 Benefit 2: “A potential reduction in administrative costs due to less frequent audits…”

It is very hard to see where significant savings could come from:

- Auditing 3 years’ data at once requires examining exactly the same set of transactions as for three one-year audits. The fact that the audit frequency has changed just means that SMSFs will receive one bill instead of three, but the total cost over three years must be at least as high.

- Audit fees are themselves not a major cost for most SMSFs. Even if some cost saving were to be achieved, its magnitude could only be trivial.

- There are some obvious ways in which audit costs must increase under this proposal:

- Both accountants and auditors will find it more difficult to manage a mixture of clients on 1-year, 2-year and 3-year audits, rather than having everyone on a 1-year cycle. This must push costs up for all clients, not just those who opt for three-year audits.

- Resolving errors, or even simple ambiguities, in data which is 2 or 3 years old will be more difficult, and therefore more costly, than when all data is no more than a year old and issues are still top-of-mind.

3.1.3 Benefit 3: “An incentive for SMSF trustees to submit SARs in a timelier manner”

The only benefit offered is the unsubstantiated hope that some cost savings will result, but even if that turns out to be true the savings will be small.

Such a nebulous offer is most unlikely to influence the trustee who has already indicated a disdain for fulfilling obligations on time and an indifference to potential penalties.

Late submission is really an administrative issue for the ATO, and it is something the ATO must face with every function it supervises. Complicating the audit cycle for SMSFs is not the way to deal with it.

3.1.4 Concern 1: “… increased non-compliance …”

Certainly the risk of inadvertent non-compliance is increased as discussed above.

The risk of deliberate non-compliance may also increase, because a more complex operating environment creates opportunities.

3.1.5 Concern 2: “… alter the workflow of the SMSF audit industry … lead[ing] to a reduction in the number of businesses specialising in SMSF audits”

That certainly seems likely, and if it occurs the reduced competitive forces will probably push audit costs up further across the market.

3.1.6 Mitigation: “… concerns will be mitigated by appropriate eligibility criteria and, if necessary, transitional arrangements”

I doubt that either eligibility criteria or transitional arrangements will address concerns about cost increases and complexity.

3.2 Do you consider an alternative definition of ‘clear audit reports’ should be adopted? Why?

Clear audits and timeliness are proposed as the criteria by which SMSFs would qualify for a three-year audit cycle.

There is an implied assumption here that SMSFs with a history of clear audit reports and timely submissions are more likely than not to continue that behaviour. Intuitively that seems likely, until one considers the very high number (40%) of SMSFs that the ATO says reported late in a three year period. The assumption ought to be tested, and I assume that ATO has the data to do so.

If one were approaching this problem for the first time, without preconceptions, one might expect that the simplicity of an SMSF’s structure and its transaction history would be a far better predictor of whether or not it routinely submits on time and receives clear audits.

However, simple SMSFs are cheaper to audit, reducing the potential (if any) for cost savings.

3.3 What is the most appropriate definition of timely submission of a SAR? Why?

I think it is consistent with the spirit of this proposal to require “timely submission” to mean three consecutive years without a late submission.

3.4 What should be considered a key event for a SMSF that would trigger the need for an audit report in that year? Which events present the most significant compliance risk?

I don’t have a view on what should constitute key events, as I think that requires a professional opinion, but the following principles are critical from a trustee’s point of view:

- The list of key events should be confined to items which, if not audited promptly, may cause serious problems later.

- Procedures should be put in place to ensure that the list of key events is kept as stable as possible, and is not allowed to grow unnecessarily.

- If trustees are to be responsible for self-assessment of their eligibility for 3-year audits, then it is essential that

- key events do not include events which are outside the trustee’s control

- key events do not include events of which the trustee may be unaware

- key events are easily understood by trustees

- it is easy for trustees to keep up to date with the list of key events

3.5 Should arrangements be put in place to manage transition to three-yearly audits for some SMSFs? If so, what metric should be used to stagger the introduction to the measure?

Although I do not support the proposal, if it does become law then the method of introduction of the process should be a business decision for accountants and auditors.

Trying to impose some system (like odd and even number plates in a fuel shortage?) seems likely to make a complex issue even more so.

3.6 Are there any other issues that should be considered in policy development?

The superannuation regulatory environment is excessively complicated and has become severely unstable: grandfathering has been virtually abandoned and frequent changes have become the order of the day, in an area that is supposed to guide investment and income provision on a generational timescale. Such instability is not in the national interest.

In this environment the only way to avoid serious unintended consequences of proposed changes is to engage in a thorough process of socialization before they are introduced. To that end, discussion papers such as the present one are very valuable, and I appreciate having had the opportunity to contribute.

The rider I would add to that, though, is that it would have been far better – from both a political and a process point of view – to have had this public discussion before the Budget announcement, rather than after it.

4 About the author

Jim Bonham is a retired scientist and manager. He is deeply concerned about the way retirement funding has developed in recent years, particularly with respect to frequent changes in superannuation legislation made with inadequate consultation and no respect for grandfathering.

Strategies to reduce your total superannuation balance: Part 3

Joseph Cheung (jcheung@dbalawyers.com.au), Lawyer and William Fettes (wfettes@dbalawyers.com.au), Senior Associate, DBA Lawyers

Due to the importance of total superannuation balance (‘TSB’) testing under the major superannuation reforms, fund members have a strong incentive to carefully monitor their TSB over time and plan accordingly to moderate their TSB to fall within certain key thresholds.

In part 1 of our series, we discussed the various components of a person’s TSB and we examined how making pension payments and/or lump sum payments could reduce a member’s TSB. In part 2 of our series, we examined paying arm’s length expenses to reduce a member’s TSB.