Scott Morrison has given a strong signal he is no longer wedded to increasing the super guarantee to 12 per cent, acknowledging it could suppress wages and potentially cost jobs, as the government weighs up the findings of an independent review into retirement incomes

The Prime Minister on Friday noted the coronavirus pandemic was a “rather significant event” which had occurred since he pledged at the last election to continue with the scheduled increase in the super guarantee, due to reach 12 per cent by 2025.

On Friday, Reserve Bank governor Philip Lowe warned that increasing the super guarantee would “certainly have a negative effect on wages growth” and that, if it went ahead, he would “expect wages growth to be even lower than it otherwise would be”.

Dr Lowe argued there could be flow-on effects if the guarantee was increased, telling the standing committee on economics it might reduce take-home pay, cut spending and potentially cost jobs.

Mr Morrison later said he was “very aware” of the issues raised by Dr Lowe and argued they should be “considered in the balance of all the other things the government is doing”.

The warning from Dr Lowe came as an inquiry heard that nearly three million Australians had applied for early access to their superannuation, with $33.3bn already approved. Labor has accused the government of undermining the superannuation system through the early access program, with Anthony Albanese warning that too many young Australians had exhausted their super balances.

Dr Lowe also criticised the states for not carrying their “fair share” of the fiscal burden, saying they were preoccupied with their credit ratings rather than job creation. He repeated the RBA’s baseline forecasts for the unemployment rate to reach 10 per cent by the end of the year and expected the jobless gauge to “still be around 7 per cent in a few years’ time”.

“The challenge we face is to create jobs, and the state governments do control many of the levers here,” he said.

Mr Morrison seized on the call to say the federal government had done the “seriously heavy lifting” to navigate the pandemic and urged state and territory leaders to “provide further fiscal support”. He said the states had provided “about $45bn in both balance sheet and direct fiscal support” but the federal government had provided “about $316bn”.

Dr Lowe said that, with the cash rate at a record low of 0.25 per cent, further monetary policy easing was unlikely to gain any traction in stimulating demand. Instead, fiscal policy and structural reform would be the primary tools to carry the country through the crisis and lay the foundations for recovery.

He identified measures such as removing stamp duties — which he called a “tax on mobility” — and industrial relations reform, echoing calls from the Productivity Commission this week.

“There’s a process going on at the moment to try and make the enterprise bargaining system more flexible, so we can get back to a world where businesses and employees can get together and make their businesses work effectively, rather than be weighed down by process,” he said.

Dr Lowe warned Australians to be prepared for a “bumpy and uneven” recovery, and argued the second wave of coronavirus infections and new restrictions meant the bank was “not expecting a lift in economic growth until the December quarter”.

Limited early release of superannuation has been a part of the government’s support to people suffering financial stress caused by the COVID-19 pandemic. This has been welcomed by some but strongly opposed by others because it is seen as a corruption of compulsory saving and disruptive to super funds.

The financial implications

This paper takes a quantitative look at the financial implications of a $10k early release, for three hypothetical individuals Continue reading

Scott

Morrison may well get his wish if private equity, backed by industry

superannuation fund money, does bid for Virgin Australia, but not the

way the Prime Minister intended, which has once again politicised super.

For

the super sector, that is the problem of being the creation of

politicians that has meant being subject to their often hypocritical

whims to suit the purpose of the day. A few weeks ago the government

thought it was clever opening the way for people to withdraw money early

from their superannuation.

Josh Frydenberg noted “it’s your money” so you can get access to it if you are caught in a financial mess because of the government-imposed shutdown.

When the industry

funds said they could face losses of up to $50bn in cash withdrawals,

the Minister for Superannuation, Jane Hume, saw it as another leg in the

push to consolidate superannuation funds.

Hume

argued that some funds like Hostplus and REST were too reliant on the

hospitality and retail sectors and, like others, had a concentrated pool

from which to raise funds because industry fund contributions were

often tied to industry industrial relations awards.

Diversification, she said, should be the rule in membership and investment strategy.

Then

Morrison came up with the bright idea that specialist industry

superannuation funds had plenty of cash so someone like the TWU, with a

heavy dose of Virgin Australia workers, should be diverting funds into

the airline.

The

three pronouncements from the relevant ministers underlines the

political bias against industry funds, breathtaking hypocrisy and, more

importantly, a dangerous ignorance about how funds manage their money.

By

law, managers must invest for the long term to boost member returns and

this fiduciary duty would by definition prevent a fund making a

national interest investment because that would suit the prime minister

of the day.

When

the government opened the door to early withdrawal of funds last month

it not only risked members losing up to $84,0000 in lifetime savings but

risked the funds losing the ability to invest to support corporate

Australia.

Somehow all of this was forgotten by Morrison.

That

said, it would not surprise if an industry fund like AustralianSuper

provided capital to support a private equity bid for Virgin.

AustralianSuper

has a stated policy of owning bigger stakes in fewer companies, which

is why it backed BGH’s successful bid for Navitas and unsuccessful bid

for Healthscope.

AustralianSuper

investment chief Mark Delaney is keen to use the fund’s equity

investments to support Australian companies with long-term capital.

This would be most company boards’ dream come true.

It would help if Canberra maintained a more consistent approach to superannuation even amid these extraordinary times.

There has been an unprecedented spending initiative by the government to prop up the economy and its citizens through a virtual shutdown for the next six to 12 months. But although self-managed superannuation funds (SMSFs) will probably be hit hard through this crisis, we’re not hearing much about help for them.

An SMSF retiree’s asset balance is vital because it is from this that future income

is generated to help fund living costs and expenses. Periods such as

this can cause great anxiety while doing irreparable damage to future

income streams as asset values plummet, particularly if there is a

prolonged period of volatility.

Compounding the stress is that many retirees were lured to the sharemarket because there was nowhere else to generate a reliable income stream. But in the recent wave of dividend deferrals and cancellations, dividend-income expectations are being cut significantly.

The Australian Prudential Regulation Authority (APRA) delivered a

regulatory mandate to cut dividends as it cautioned banks and insurance

companies on paying out too much in dividends. This relief lever was seized quickly by the Bank of Queensland at the time of its half-year result.

Unlike share prices that are subject to sentiment, dividends paid by a company tend to reflect the economic reality a business faces. With declines in profitability and free cash flow expected for the coming six to 12 months, the income reality from the sharemarket for retirees on a risk-adjusted basis is bleak.

The outlook for other asset classes in which SMSFs traditionally invest doesn’t look much better. The property market is at risk of seeing its income dry up, leaving many retirees in the lurch. With the rising call for government-mandated rent deferrals, the SMSF property investor who previously received 4 per cent rental returns is likely to be affected significantly.

Further, investors in property trusts, exchange-traded funds (ETFs)

and listed and unlisted funds could face a freeze on their distributions

should conditions and asset values deteriorate further.

And

let’s not forget those who sought the safety of cash and term deposits

in the recent turmoil – $1 million held in cash-like products returns an

absolute maximum $15,000 a year, well below the regular JobSeeker

payment. With interest rates to remain lower for much longer, there is

little in the way of hope.

Huge fall in earnings

Should

economic and investment conditions worsen, an SMSF retiree could

potentially see earnings fall by well over 60 per cent. For SMSFs on the

margin, this could fall well below the age pension and JobSeeker

payment level.

According to the SMSF Association, there are

560,000 SMSFs comprised of 1.1 million members. The Australian Taxation

Office (ATO), in its last published SMSF quarterly statistical report

for the three months ended September 30, showed that 37.1 per cent of

all SMSF members were of retirement age, which equates to more than

400,000 individuals.

The federal government’s decision to reduce

the minimum SMSF pension withdrawal requirement by 50 per cent is

important – particularly as this amount is calculated based on the asset

value at the start of the financial year.

But another part of the government’s support package was to drop the deeming rate used in the income test to determine qualification for financial support such as the age pension. Without going into the technicalities, the decrease in deeming rate means a reduction in accessible income that would result in those who receive a part pension being able to receive more and, in theory, potentially help some SMSF members on the margin to be eligible for at least a part pension.

The statistics, however, show that for SMSFs, this will probably not

be the case. In the ATO report, while there is no breakdown as to

whether the SMSFs are in accumulation or pension phase, the median

average balance of all SMSFs per member was $408,237. The reality is

that older SMSF members tend to have larger balances and therefore would

most likely be disqualified from receiving the age pension as they fail

the assets test.

Before this correction, an SMSF retiree couple

with $1.2 million between them, who owned their own home and earned an

income of 5 per cent on a balanced portfolio of assets, would derive in

total $60,000 income for the year ($2307 a fortnight). A 60 per cent

drop in future income results in $923 a fortnight, which is more than

$370, or 30 per cent, less than the age pension.

Of course, where

asset values do fall below the upper asset threshold ($869,500 in the

case of a married couple who own their own home), they will qualify for a

part pension under the current rules. But it is important to note that

asset values in property and unlisted trusts often lag, with

revaluations conducted sparingly.

Although the income hit of

suspended distributions will probably be felt early, any asset revalue

relief from non-shares assets may be some time in coming – supporting

the idea of immediate income support in the near term.

SMSF

retirees who fail the assets test will have no option but to dip into

their savings, rendering the government drop in the minimum pension

withdrawal level totally useless. This drawdown will result in a lower

asset base for future income generation, making it more difficult for

them to be self-sustaining and increasing the future burden on

government.

Short-term assistance

For the

same duration that JobSeeker, JobKeeper and other spending initiatives

are implemented, a possible aid package to SMSF retirees might include

the assets test being waived and a regular ongoing payment equal to a

minimum of 50 per cent of the current full age pension.

Although

this in a few cases may still fall short of past income levels, it

would provide urgent short-term income relief. It would reduce the need

for excess drawdowns on assets when prices are challenged and/or

liquidity dries up.

Further, for those who under normal

circumstances pass the assets test, but receive a part pension due to

other income generation, for the same period they could automatically be

eligible for the full pension to compensate for loss of income.

The

main intention would be to deliver some basic support to the large

number of forgotten SMSF members whose income even when investments were

stable was inadequate.

Murray, who was chief executive of the Commonwealth Bank of Australia for 13 years and is now chairman of wealth manager AMP, says it is actually misleading to call it a retirement income system.

“Ours is not a superannuation system, it’s a tax advantaged savings system,” he says.

Murray says the fact that thousands of Australians have, in recent weeks, rushed to switch out of balanced funds into cash after the stockmarket had fallen by about 38 per cent was an indication the system was not fit for purpose.

He says Australia should mandate the payment of a pension to super fund members upon retirement. This would make the job of super fund trustees easier because they could match long term assets with long term liabilities.

Murray says the final report of the FSI delivered to the federal

government in November 2014 recognised the impossibility of politicians

agreeing to Australia introducing mandated pension payments upon

retirement.

As a simpler and more politically acceptable option,

the FSI recommended the introduction of Comprehensive Income Products

for Retirement (CIPRs).

Annuity-style pension products

“We

made recommendations about an annuity style product called CIPRs, which

would try and encourage people through self-selection to focus more on

annuity style pension products in retirement,” he says.

“The

issues that we discussed around the CIPRs started with the discussion

about what does a really good system look like. And apart from having a

retirement income objective for the system, a really good system would

only pay pensions in the form of annuities. That is a pension should

provide a pension.

“That would create a much more predictable environment for trustees to manage risk and asset allocation.

“The

reason we didn’t recommend that pensions be mandated was that we’re in a

country that if it had been promoted it would have been easily

politically defeated. So, we fell back on the simpler recommendation.”

Of

course, the federal government has dragged the chain on implementing a

comprehensive tax efficient framework for CIPRs. It is not the only area

where the FSI recommendations have been half heartedly implemented or

ignored.

Murray is disappointed that legislation defining the

single objective of super as being for retirement income has not passed

through parliament. He thinks independent trustee directors should be on

industry fund super boards. But the government has given up on this

fight after repeatedly failing to get such measures through the Senate.

The single most important recommendation of the FSI was in relation to the need for the big four banks to be “unquestionably strong”. This was implemented by the Australian Prudential Regulation Authority.

As a result of this measure the big four reduced their leverage and

implemented common equity tier 1 capital which Commonwealth Bank of

Australia CEO Matt Comyn this week said was the strongest in the world.

Murray

says “unquestionably strong” has “worked nicely” but he is concerned

that the super system, which should be a force for stability in times of

crisis, is in need of emergency liquidity from the Reserve Bank of

Australia.

Funds don’t need RBA support

The switching out

of growth assets into cash over the past two weeks combined with the

federal government’s decision to allow emergency access to $20,000 in

super savings has prompted several leading industry super funds to

request RBA support.

Superannuation minister Jane Hume has

rejected the idea and suggested any fund unable to pay its members must

have poor governance of its investment strategy.

Murray, too, is

damning in his commentary of any fund that is need of liquidity. He says

the root of the problem is funds advertising on the basis of having a

higher rate of return

“The discussion about switching does show

the flaw in this system where you can keep changing your allocations and

it shows some of the systemic risks that arise,” he says.

“I

think the more serious issue is that where superannuation is advertised

and sold on the basis only of rate of return, then trustees will make

assumptions and seek out the highest rate of return in their asset

allocations with some risk to stability as they go forward.

“By assuming that default funds will flow in no matter what, that the inflows will keep rising and that therefore funds can take more risks with the illiquid assets

means these funds are establishing a higher risk system for their

members. And this is what has shown up recently to the point where the

funds want liquidity support.

“Now, whether that is simply because

the government has allowed some early withdrawals or not, only each

fund knows, but on the amounts that the government has mentioned, it

seems to me to be not quite credible that a well-managed fund should

need support for those amounts of withdrawals.

“If we have funds

that have taken aggressive asset allocation positions, have sold those

on the basis of rate of return for their default fund and attracted

money from other funds as a result, then the funds that have taken a

more cautious approach are penalised and their own members could well be

penalised.

Take cue from Singapore

“Now, we can’t solve

that now because the role of the government and the Reserve Bank is to

manage the crisis we’ve got. But it does demonstrate that this system we

have is not right. And I think we have to face into some more sensible

arrangements for the future than we have today.”

Murray warns

against the RBA stepping in to provide liquidity to super funds because

of the moral hazard. But he says if emergency support is required then

we could copy Singapore’s Temasek-style sovereign wealth fund.

He

says this fund could acquire assets from a fund needing liquidity but

in doing so the fund would have to accept a price in alignment with the

prices prevailing in the sharemarket.

The government owned entity

could purchase assets from the super fund in return for liquidity and

this would allow the fund to restore its asset allocation back to the

level which prevailed before the COVID-19 sell-off.

Murray says

this would be fair to all members of a fund because the illiquid assets

would have to be sold at a discount to face value. The alternative is

inequity for members in the fund not switching to cash because they

would be stuck with overvalued assets.

Murray says that by matching the price of assets to the general movement in equities in the market plus a further discount for illiquidity would mean the government entity buying the assets would pay fair value.

The assets could be sold later and the taxpayer would make a profit.

The concept of a Temasek style sovereign wealth fund would suit the

times given the need for the government to bail out Virgin Australia.

Temasek,

which owns 55 per cent of Singapore Airlines (which in turn owns 23 per

cent of Virgin), last week underwrote a $S5.3 billion ($6.1 billion)

equity raising by Singapore Airlines. The airline also raised $S9.7

billion through the issue of 10-year bonds.

Murray says he is inclined to think the banking system is fine given it has no systemic prudential issues.

“On

the other hand, there are some fundamental issues in superannuation

that we can get through with some support if it can be designed the

right way and we don’t create this moral hazard for the future,” he

says.

“But then we have to open up the way this damn thing works and fix it.”

Many

people are recycling Warren Buffett’s famous quote that it’s only when

the tide goes out that we discover who has been swimming naked. And for

good reason: one Australian industry is looking pretty ugly right now,

its mismanagement and hubris exposed by this current crisis. The naked

swimmers are the trustees of the biggest industry superannuation funds

and their directors.

This sector

rode so high and mighty in the good times that it demanded that the

corporate sector, especially the banks, take money from their owners

and give it to causes deemed worthy by these industry super funds.

In the midst of this crisis, while the banks are honourably bailing out their customers, these sanctimonious industry super funds demand that ordinary Australians rescue them and their members from the consequences of the sector’s arrogance.

The biggest question is how this group has

been protected from scrutiny and sensible regulation for so long, and

what can be done to end its immunity from the kind of critical

examination the rest of the financial sector has always faced.

Consider

the causes of the arrogance and power of large industry super funds.

They have been coddled by an industrial relations club that mandates

that it be showered with never-ending torrents of new money. Of the 530

super funds listed in modern industrial awards, 96.6 per cent are

industry super funds. That’s some gravy train.

With that guaranteed inflow of cash, it’s hardly surprising that industry super funds have grown fat and lazy about risk. They made two critical assumptions. First, that these vast inflows would always exceed the outflows they had to pay pensioners and superannuants. And second, they could keep less of their assets in cash or liquid assets to meet redemptions.

In fact, they doubled down on this bet by

plunging members’ money into illiquid assets — they filled their

portfolios with infrastructure, real estate, private equity and other

forms of long-term assets that can’t be easily and quickly sold to meet

redemptions.

These assets can’t be

easily valued either — experts will tell you that the valuation of

illiquid assets is essentially guesswork. If you don’t have a deep and

liquid market into which to sell an asset, you really have no idea what

that asset would fetch if and when the time came to sell.

The fact the valuation of illiquid assets is open to huge variation was a terrific advantage in so many ways for industry insiders during the good times.

Industry super funds could use boomtime

assumptions to produce inflated valuations to prop up their performance

relative to retail funds that don’t have the same guaranteed gravy

train of inflows to invest in unlisted long-term asset classes.

That

gives the industry funds one heck of a competitive edge and those

inflated performance figures make for handsome bonuses for employees

of industry funds and asset managers such as IFM.

This

apparent outperformance by industry super funds seems to have

anaesthetised the Australian Prudential Regulation Authority and many

others. They have been able to resist sensible regulation by pointing to

their “healthy” performance, and they have received exemptions from the

kind of stock-standard rules that govern other trustees of public

money.

The upshot is that many industry

super funds have ridiculously large boards stuffed full of union or

industry association nominees who obligingly pass their directors’ fees

back to their nominating union (where, lo and behold, it might find its

way to the ALP) or industry association.

But

now the music has stopped. What these big industry funds have sold to

members as “balanced” funds doesn’t look so balanced any more.

The

current crisis has exposed illiquidity issues. Many of their members

have lost their jobs or lost hours of work, drying up the guaranteed

flow of new superannuation contributions.

And

the Morrison government has announced an emergency and temporary

exemption allowing members in financial trouble to withdraw up to

$10,000 a year from superannuation for each of the next two years.

The

liquidity problem facing industry super funds has been compounded by

the fact many members have been switching from what the industry funds

call “balanced” options into cash options, requiring funds to liquidate

long-term assets in the “balanced” options.

This

new environment has forced industry funds to slash questionable

valuations of illiquid assets in their “balanced” funds to avoid

redeeming members or members who switch out of balanced funds into cash

options getting a windfall at the expense of members who remain in the

“balanced” funds.

So the jig is up.

When comparisons between industry super funds and retail funds are

adjusted for risk — as they should be — industry super funds don’t look

so healthy after all.

Now that the tide

has gone out, we can see two issues with greater clarity. First,

trustees of industry super funds haven’t done a stellar job of managing

risk through the full economic cycle, through good times and bad.

There

was too much complacency from more than two decades of uninterrupted

economic growth. And maybe some naivety too: Australian industry funds

are relatively new, emerging only in the 1980s after the introduction of

compulsory superannuation payments.

Second,

APRA stands condemned for letting industry super funds get away with

second-rate governance and poor management of risk through the full

economic cycle.

Consider the hypocrisy

of these super funds now wanting a bailout to deal with a liquidity

problem of their own making during the boom times. For years, noisy

industry funds have sanctimoniously demanded that company boards give up

some profit to benefit society.

Now

their mismanagement has exposed risks that their members may not have

been told about. And the same industry funds want the Reserve Bank of

Australia (aka the taxpayer) to bail out their members to protect their

boards from claims of mismanagement. The industry funds no doubt will

point to the help the government is giving the banks as a precedent for

a bailout.

However, they should

remember that the quid pro quo for banks getting government help is the

banks meeting a stringent set of capital and liquidity rules, not to

mention governance requirements such as a majority of independent

directors. Do these funds want a similar regime instead of the

namby-pamby one that applies now?

To

date, and to its credit, the Morrison government has resisted their

calls. Scott Morrison and Josh Frydenberg should stand even stronger,

demanding APRA lift its game. How did the industry fund sector escape

scrutiny of its dirty little secrets for so long?

Part

of the reason is sheer thuggery. Industry Super Australia, the

representative body for industry super funds, tried to silence Andrew

Bragg a few years ago when he was at the Business Council of Australia

for exposing the unholy links between unions and industry fund. Bragg,

now a senator, is leading the push to reform industry super.

The

voting power, and buying power, of huge industry funds is another part

of the answer. Their special pleading and scare tactics to ensure they

can keep feasting on members’ funds by having the super guarantee charge

contribution increased from 9.5 per cent to 12 per cent is the rest of

the answer.

The pathetic plea for a

taxpayer-funded bailout from mismanaged industry super funds is

compelling evidence that workers should be allowed to keep more, not

less, of their hard-earned money rather than be forced to shovel more

into industry funds and their mates.

The young and poor have little say in society but they are incurring the bulk of the costs from the shutdown.

Whether

it’s their incomes, their schooling or their ability to enjoy life, the

sacrifices that students and so-called generations X and Y are making

for the over-75s are very significant. Unlike the Spanish flu 90 years

ago, it seems coronavirus is of little threat to the vast majority.

The $320bn the government and Reserve Bank have allocated so far to staunch the self-imposed economic carnage will have to be paid for. The plunge in tax revenues could well be as significant as the increase in outlays, leaving a gap that will test governments’ ability to borrow. There’s already $400 trillion of debt sloshing around the world.

And the bill will come long after those

whom the younger generations have tried to protect have died. It’s

reasonable to give some thought now to how the costs will be shared.

Policies

that were thought fair and reasonable only months ago will start to

look unfair, even absurd. The government will face stark choices about

how to allocate the burden. Will it crush the productive sector of the

economy with even more income tax?

Everyone will suffer in degrees during this crisis, but it’s only fair that those who are being saved, especially if they are financially equipped, pay a disproportionate burden of the cost.

(It’s true retirees have seen huge falls

in their superannuation balances, but once a vaccine is found in a year

or two, their accounts are likely to roar back to life.)

The

Commonwealth Seniors Health Card, which is a benefit for retirees who

are too well-off to quality for the Age Pension, should be immediately

dumped.

How can we have people queuing

up for soup in Sydney’s Martin Place (as was the case on Sunday night),

while taxpayers fork out hundreds of millions of dollars a year to

ensure cheap medicines and transport for those who can easily afford

them anyway?

Scrapping the seniors and

pensions tax offset, which provides a tax-free threshold of about

$33,000 for over-65s and about $58,000 for couples, is also a

no-brainer. Naturally, these two changes will cause some discomfort for

those affected, but nothing compared with the chaos recently foisted on

millions.

It’s obvious the superannuation guarantee should be suspended for the rest of the year, as I’ve argued repeatedly. The government is forgoing almost $20bn a year in tax by keeping it when it needs the revenue urgently.

Coronavirus: Economic bailouts

Country

Bailout amount

Additions

USA

$A3.2 trillion

+ $A810bn for layoffs

Germany

$A1.3 trillion

+ $A89bn for layoffs

UK

$A627bn

+ 80% of salaries up to $2390/month for layoffs

Japan

$A437bn

+ cash payments and travel subsidies for layoffs

Australia

$320bn

+ workers and sole traders can access $10,000 tax free from superannuation, + $1500 per fortnight for workers

Canada

$A121bn

+ $2000/month for 4 months for layoffs

South Korea

$A66bn

Norway

$A15.2bn

+ 100% of salary for 20 days / 80% if self-employed for layoffs

New Zealand

$A11.5bn

+ wages covered for people who need to self-isolate

As of March 31, 2020

Rather

than taxing younger generations or workers to oblivion, it’s best to

curtail generous arrangements, at least temporarily. These tax increase

would have relatively little or no impact on disposable incomes;

indeed, in the case of suspending the super guarantee, take-home pay

would increase for millions of workers.

Other

options might include a significant inheritance tax imposed, say, for

the next 20 years to help defray the gargantuan tax burden that has just

been put on everyone who is not going to die in that period.

Tax-free

earnings on superannuation in the retirement phase should cease, at

least temporarily. Currently, the earnings of superannuation funds for

retirees face zero taxation.

Everyone

else pays 15 per cent tax. It should be the same for everyone (as the

Henry tax review recommended, by the way). Fifteen per cent is still a

lot more generous than marginal income tax rates.

Cancelling the refundability of franking credits — for everyone, not just self-funded retirees — is another option.

To

be sure, this would cause real pain, given some retirees quite

reasonably have structured their affairs around them. But this is a

crisis.

There are some economic bright

sides for younger people. If a house price crash eventuates, those with

jobs and to obtain credit will be more easily able to afford a home.

Whether

house prices fall for long remains to be seen, though. In times of

uncertainty, gold and property tend to be relatively attractive assets

and immune from inflation.

And

significant inflation may well be on the horizon. The borrowing lobby in

society is much more politically powerful than the lending lobby. That

is, the constituency that benefits from inflation (anyone with debt) is

greater than those who wouldn’t.

What’s

more, a niche group of economists reckons the central bank can give us

all money directly — say, $10,000 each straight into our bank accounts —

without undermining the economic system.

It’s known as Modern Monetary Theory and, understandably, it is becoming popular.

“There’s

no such thing as a free lunch” was branded into me through years of

economics study. It’s hard to imagine that we can just make new money

out of thin air without serious long-term costs to the economic system,

or certainly respect for it.

Why would anyone bother working or saving?

The

fiscal situation is looking so dire a future government might well give

MMT a try. It’s so seductive. They should be wary, though. A great

inflation has unpredictable consequences, which history suggests can be

terrible.

Nevertheless, if inflation

does break out, the burden of the economic shutdown would play out very

differently. It would remove the government and private debt burden,

obviating the need for the various tax increases suggested above. Anyone

with significant cash or deposit holdings would be wiped out.

For now, however, this is all academic.

As

in an ordinary war, the young are doing the heavy lifting and face a

massive tax burden. It could be a bit less burdensome if reasonable,

temporary tax increases were imposed for the over-65s to help defray the

costs.

It’s important to keep perspective. Roughly 165,000 people die in Australia each year; about 3000 from influenza.

Meanwhile, the economy is being destroyed — real and permanent damage — for uncertain benefit.

If

we totally shut down the economy, as many are advocating, when does it

reopen? And if it reopens and the virus emerges again, is it shut down

once more?

It’s patently not possible to keep turning an economy on and off every few months without destroying civilisation.

Between now and

2025 the compulsory “superannuation guarantee” (SG) contribution to superannuation

is legislated to increase in steps from 9.5% of gross income to 12%.

Unfortunately,

formal “think tank” and academic reports tend to be inaccessible to the average

reader. Calculations may be opaque; and journalists often

manage to make the impending increase look quite complicated and confusing.

It does not have to be so. This short note explores the immediate consequences of the legislated increase in the SG rate from 9.5% to 12% and introduces an alternative proposal to increase the SG rate to 10%, or even leave it unchanged, and drop the contribution tax entirely.

The table below

lists what I perceive to be the main points of concern, and a brief comment on

each. This is provided for context, not

as a detailed commentary on any specific position.

Perceived problem

Comment

(a)

Retirees already have enough money so there is no need to beef up super.

Depending on investment returns, current SG contributions will only provide an initial retirement income of 14% to 25%, or so, of final employment income (depending on investment choices).

(b)

Increasing the SG rate will depress incomes.

The government has reportedly asked ANU to advise specifically on this issue. Gross incomes will fall by 2.23% (given assumptions detailed in the text), but there is an alternative.

(c)

Increasing retirees’ assets will disproportionately reduce their age pension entitlement

This reflects a problem with the structure of the age pension, not super. In any event it will take a decade or so to become significant, leaving plenty of time to fix the structural issue.

(d)

The budget can’t afford the cost

The cost to the government of the planned increases, per employee, is equivalent to about 0.5% of their gross income – the equivalent of a modest tax cut.

Each of these

issues is discussed in more detail below.

The intention is not to provide detailed rebuttals of any specific point

of view, but rather to add context to the upcoming increase, and to suggest an

alternative approach.

3 How much does the SG provide?

It can be a

daunting task to work out how much superannuation one will have in retirement,

what its real value will be and how that might relate to one’s income needs.

Fortunately, help

is available from on-line calculators such as the excellent one provided by

ASIC (https://moneysmart.gov.au/how-super-works/superannuation-calculator) which also provides detailed actuarially

determined estimates of long term investment returns, fees and earnings for

several common investment styles, as well as estimates of inflation and wages

growth (as reflected in rising living standards).

A common measure,

used by the OECD for example, for assessing retirement funding systems is the

replacement ratio, which is the initial income in retirement divided by the

final employment income. (Obviously,

this only makes sense for someone who remains in steady employment up to

retirement and doesn’t apply to those with a more fractured employment

history).

It is generally

accepted that a replacement ratio of 70% represents good practice and, in the

absence of better information, it seems to “feel” about right.

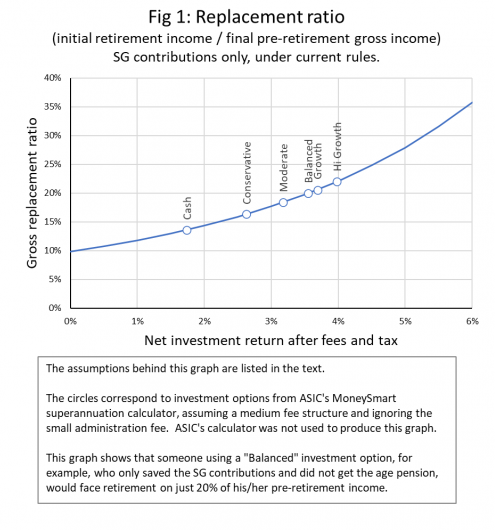

Fig 1 shows the

replacement ratio expected just from current SG contributions and their

compounded investment returns, assuming

SG rate is 9.5%, taxed at 15%

Wages growth is 3.2%

Length of employment is 45 years

On retirement, superannuation is converted to an allocated pension from which 5% per annum is drawn as income in the early years.

Complications such as contribution caps are ignored.

The simple conclusion from Fig 1 is that, however the superannuation account is invested, the SG contributions alone will not provide anything like a 70% replacement ratio.

Most people will

need to supplement their SG contributions substantially with further voluntary

superannuation contributions, the age pension, or other investments outside

superannuation, in order to live at a level anything like what they were used

to.

There is thus a lot

of scope to increase the SG contributions, which goes a long way toward

refuting Issue 2(a).

4 How will the SG rate increase affect pre-retirement

incomes?

To keep things simple, we’ll exclude from

consideration those who are on a very low income, those who are subject to Division

293 tax (incomes over $250,000) and those who are already at or near the

concessional contribution cap. We’ll also assume that all income derives from

employment. Finally, in the interests of

simplicity, we’ll assume that the increase takes place in one step rather than

being staged over several years.

It is highly likely that employer bargaining power

is such that increasing the SG contribution rate will not affect total income

packages (i.e. gross income plus SG contributions). The calculations below assume that this is so

– it is a key assumption of this paper.

Note, however, that in real life salary

negotiations are not necessarily cut and dried.

So, a push to restore a previous total package value might not be

immediate but be buried in subsequent increments, or it might manifest as

additional pressure in future negotiations.

To be able to work this through mathematically,

however, we make the simplifying assumption that incomes will adjust

immediately.

It’s also important to keep in mind that while a

mathematical model produces precise, neat and tidy results, these are only as

good as the initial assumptions – the real world is much messier. The important function of an analysis such as

this one is not so much to produce precise predictions, but rather to lay bare

the way in which key variables (in this instance: income, income tax, SG rate and

contribution tax) all interact. Better

understanding should lead to better decision making.

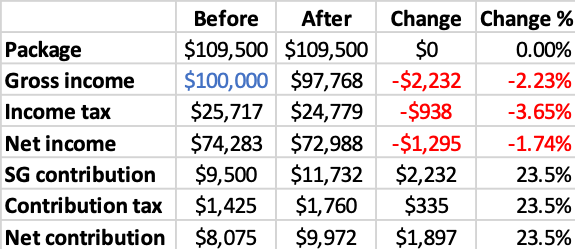

With these cautions in mind, let’s move on. Some straightforward arithmetic, illustrated

in Table 1, shows that the immediate consequences of increasing the SG rate will

be as follows:

SG

contributions will rise by 23.5%

Gross

incomes will fall by 2.23%

Net

SG contributions will rise by 23.5%, corresponding to 1.90% of initial gross

income

Government

income tax receipts will fall by an amount which depends on income.

Table 1 shows how the numbers work out for an initial gross income of $100,000:

Table 1

The top line reflects the assumption of no change

in the total income package

so, there must be a drop in gross income (2nd

line)

and therefore, the government’s income tax

receipts will fall (3rd line)

as will the individual’s net income (4th

line).

The SG contribution goes up by 23.5% (5th

line).

The government claws back an extra 23.5%

contributions tax (6th line)

leaving a net contribution which is also 23.5%

higher than before (7th line).

In summary, the superannuation account of the individual

currently earning $100,000 nets an extra $1,897 per year. In the short term, this is a zero-sum game

(the savings have to be paid for): $1,295 is provided by the individual

(reduced net income offset by lower income tax) and $603 is provided by the

government (reduced income tax receipts offset by higher contribution tax).

In other words, the individual saves more, and the

government also contributes.

Although this is a zero-sum game in the short term, that is

not the case in the long term.

Superannuation savings provide a massive investment resource for the

nation, and a more financially secure retiree population will require less

government support. There is a large net

benefit to the nation from supporting and incentivising long-term saving.

Although Table 1 is worked for $100,000 initial gross

income, the same 2.23% fall in gross income and 23.5% increase in net SG

contribution occurs for any other initial income.

The boost to SG contributions then flows through to provide

a valuable 23.5% increase in the value of SG contributions and their

accumulated investment returns at any time through to retirement, and

consequently the same percentage increase in both earnings and earnings tax.

A partial response to Issue 2(b), therefore, is: yes, the planned

increase in SG rate will depress gross incomes by 2.23%.

5

How is the cost shared between government and

individual?

Before the increase, the net SG contribution is 8.075%,

after allowing for the 15% contributions tax, so a 23.5% increase in that corresponds

to 1.90% of the initial gross income. That

1.90% must be paid for, and as we have seen the cost is shared between the

individual and the government.

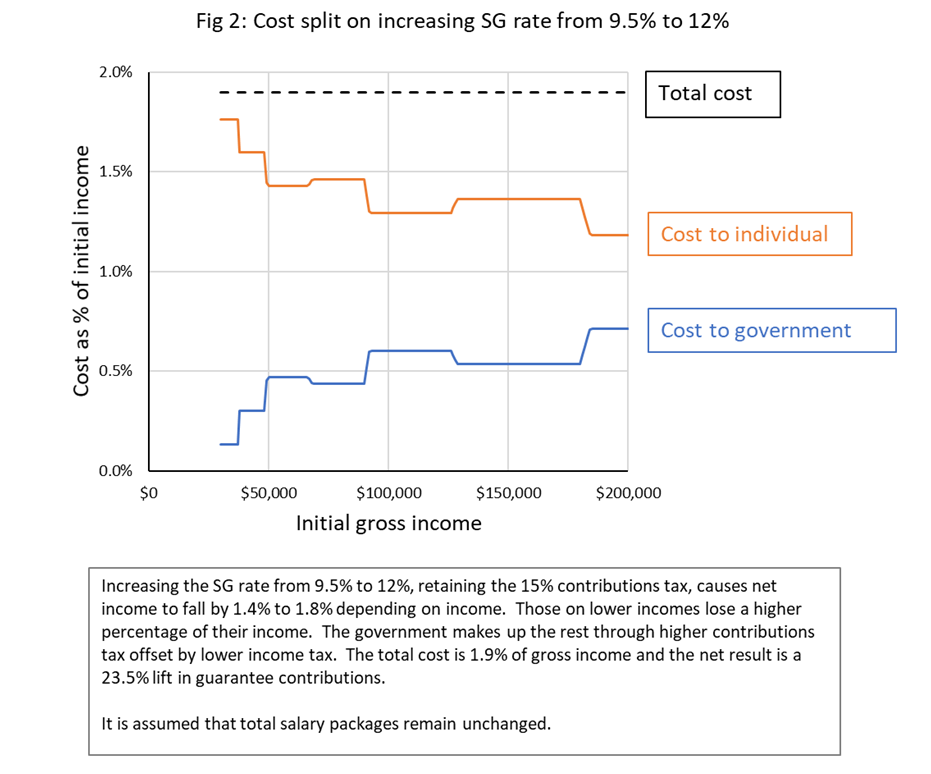

Fig 2 shows the split for a wide range of initial incomes, the structure in the graphs reflecting the complicated structure of income tax rates.

The cost to government averages about 0.5% of gross income

(for incomes between $50,000 and $180,000) and that helps put Issue 2(d) in

context: it is of similar magnitude to a modest income tax reduction.

The cost should not be onerous for the government and could

be funded by cancelling or reducing less important programs, or by working with

greater efficiency (meant literally, not as a euphemism for sacking people

which only pushes costs back to individuals).

Incidentally, the cost to government is sometimes compared

to the cost of fixing other significant problems, such as Newstart. This is the wrong way to evaluate the

priority of a project: it should be compared to the least important project,

which can most easily be dropped, not to other important projects.

6

How quickly will the effects be felt?

The effects on net income and taxes discussed above will be

immediate, but the impact on retirement income will take time to evolve – about

a decade for effects to become noticeable and four decades for the complete

benefit.

Superannuation operates over the very long term, which means

the sooner problems are fixed the better. The current financial climate does

not justify delay.

Two issues which will eventually emerge but will be

insignificant for the first couple of decades are:

Earnings taxes on superannuation investments

will increase by 23.5%.

Age pension entitlements will decrease for

people on low-to-moderate-incomes.

Both benefit the government.

However, the age pension needs significant modification to correct other

fundamental problems:

Inappropriate indexing creates inbuilt

instabilities in the age pension which will make it harder to get and less

generous in the future. This is a little-known but serious long-term structural

deficiency. See https://saveoursuper.org.au/wp-content/uploads/Retiree-time-bombs.pdf

In short, there is plenty of time and opportunity to make

sure that Issue 2(c) will not become a problem.

7

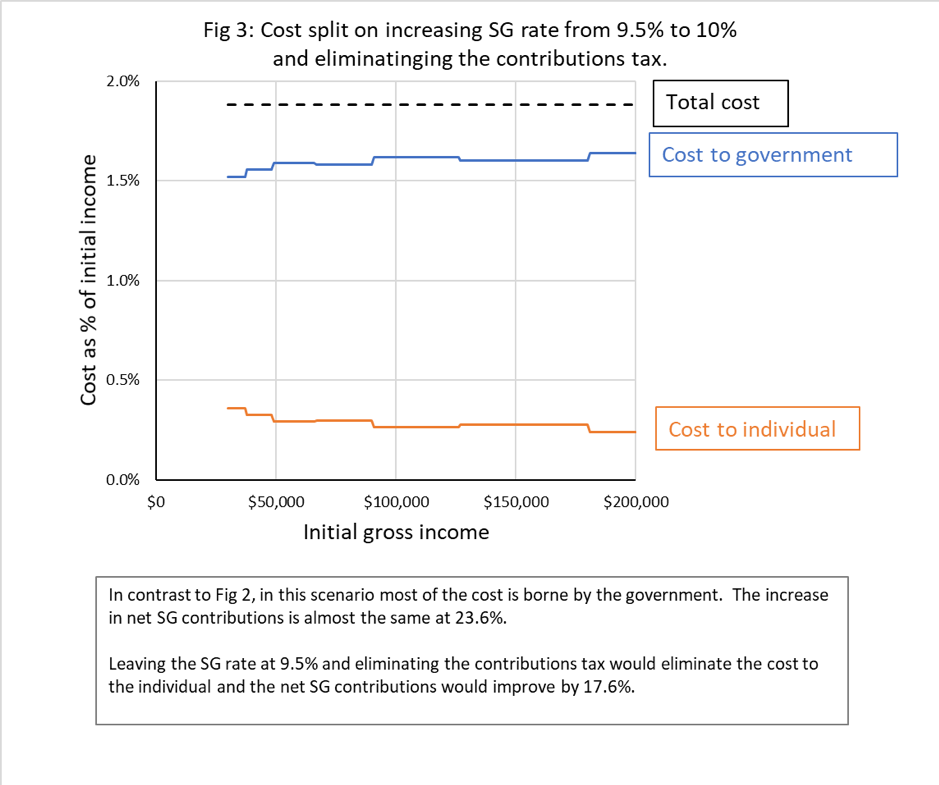

An alternative proposal

The above calculations highlight something quite bizarre

about concessional superannuation contributions: the superannuation guarantee

compels people to save for their retirement, but the contributions tax

immediately undermines that – now you see it, now you don’t!

The system would be much neater and easier to understand if

the contributions tax were abolished.

That would also make voluntary concessional contributions

(up to the cap) more attractive, thus encouraging more saving, but let’s look

more closely at what it would mean for compulsory SG contributions.

As we have seen the upcoming increase in SG rate will

increase compulsory net contributions to superannuation by 23.5%, given the

assumption that gross incomes are unaffected, so let’s take that as an

objective and see how it would be achieved without the contributions tax.

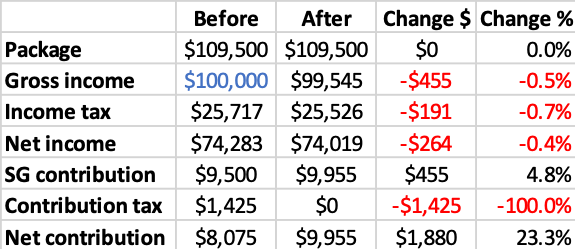

The answer is that the SG rate then only needs to be

increased to 10%, rather than 12%. Net

contributions will increase by 23.3% which is almost identical to 23.5%, but

the split in cost between the government and individual is changed

significantly.

Table 2 shows the detailed figures for a gross income of

$100,000:

Table 2

and Fig 3 shows the split in costs between government and

individual for a range of gross incomes:

From the government’s point of view, this proposal is more

expensive by about 1% of gross income than the increase currently legislated – it

is still the equivalent of a modest tax cut across the board. Staging this change over several years would

further reduce the budgetary shock.

From the individual’s point of view, the cost has reduced to

about a quarter of a percent of gross income, which in normal times most people

would not notice.

However, these are not normal times: the aftermath of this

summer’s fires and the developing coronavirus scenario mean that many people

are or will be under severe financial pressure.

The government is currently working to provide significant stimulus in

response. The government has also reportedly

asked ANU to advise the government on whether the upcoming increase will affect

incomes.

As shown above, they certainly will do so, and it is

tempting to see this as a strong argument against making any increase at all.

However, it is easy in times of crisis to neglect long term

issues, banking problems for future generations.

The government could find it attractive, therefore, to demonstrate

a continued commitment to long term saving by dropping the contributions tax,

while leaving the SG rate at 9.5% so there is no additional cost for

individuals.

If that approach is followed, the boost to net SG

contributions will be 17.6% instead of 23.5% – a little less, but still a

sizeable improvement for the long term.

To see what that would mean, we return to Fig 1 and consider

someone who chooses a “Balanced” investment option for their super. Using ASIC’s figures, that would give a

replacement ratio of 20% under the current rules for the assets derived from SG

contributions.

The initial retirement income would thus be 24.7% of final

employment income under the current plan (23.5% improvement), or 23.5% of final

employment income if the SG rate remains at 9.5% and the contributions tax is

dropped (17.6% improvement). Either way,

it is a significant improvement, while still leaving a considerable gap to be

filled by extra voluntary saving, or the age pension, depending on the

retiree’s circumstances.

8

About the author

Jim Bonham (BSc (Sydney), PhD (Qld), Dip Corp Mgt, FRACI) is a retired scientist (physical chemistry). His career spanned 7 years as an academic followed by 25 years in the pulp and paper industry, where he managed scientific research and the development of new products and processes. He has been retired for 14 years and has run an SMSF for 17 years. He will not be affected by any change to the superannuation guarantee.

The Manager

Retirement Income Policy Division

Treasury

Langton Cres

Parkes ACT 2600

Save Our Super submission:

Consumer Advocacy Body for Superannuation

Dear Sir/Madam

Save Our Super

has recently prepared an extensive Submission to the Retirement Income Review

dealing in part with the many ‘consumer’ issues triggered by the structure of

retirement income policy and the frequent and complex legislative change to

that policy.

That Submission was lodged with the Review’s Treasury Secretariat on 10 January 2020 and a copy is attached to the e-mail forwarding this letter. It serves as an example of the analysis of super and retirement policy and of the advocacy that superannuation fund members, both savers and retirees, can contribute. Its four authors’ backgrounds show the wide range of experience that can be useful in the consumer advocacy role.

We note both the

policy and the advocacy consultations are running simultaneously, exemplifying

the pressures Government legislative activity places on meaningful consumer

input. Consumer representation is

necessarily more reliant on volunteer and part-time contributions than the work

of industry and union lobbyists and the juggernaut of government legislative

and administrative initiatives.

Given the

breadth, complexity and fundamentally important nature of the issues raised for

the Retirement Income Review by its Consultation Paper, we have prioritised our

submission to that Review over the issues raised by the idea of a Consumer

Advocacy Body. This letter serves as a

brief submission and as a ‘place holder’ for Save Our Super’s interest in the

consumer advocacy issues.

The idea of a

consumer advocacy body is worthwhile in trying to improve member information,

engagement and voice in superannuation and in the formation of better, more

stable and more trustworthy retirement income policy. It should help

government to understand the perspectives of superannuation members.

Save Our Super was

formed from our frustration at the evolution of superannuation and broader

retirement income policies. We

contributed as best we could to the rushed and heavily constrained Government consultations

on, and Parliamentary Committee inquiries into, the complex retirement income policy

changes that took effect in 2017. One example of our inputs is https://saveoursuper.org.au/save-supers-joint-submission-senate-committee-two-superannuation-bills/ .

For the

consultations on the Consumer Advocacy Body for Superannuation, we limit our

comments here to point 1 on the Consultation’s brief web page, https://treasury.gov.au/consultation/c2019-38640 :

“Functions and outcomes: What core

functions and outcomes do you consider could be delivered by the advocacy body?

What additional functions and outcomes could also be considered? What functions

would the advocacy body provide that are not currently available?”

Key roles

Consult with superannuation fund members on their concerns, including issues of legal and regulatory complexity, frequent legislative change and legislative risk which has become destructive of trust in superannuation and its rule-making.

Commission or perform research arising from consultations and reporting of member concerns.

Tap perspectives of all superannuation users, whether young, mid-career, or near-retirement savers, as well as of part- or fully self-funded retirees.

Publish reporting of savers’ concerns to Government, at least twice-yearly and in advance of annual budget cycles.

Contribute an impact statement – as envisaged in the lapsed Superannuation (Objectives) Bill – of the effects of changes to any legislation (not just super legislation) on retirement income (interpreted broadly to include the assets, net income and general well-being of retirees, now and in the future).

The advocacy body should:

take a long-term view, and could be made the authority to administer, review or critique the essential modelling referred to in Save Our Super’s submission to the Retirement Income Review. Ideally, the Consumer Advocacy Body should have the freedom to commission Treasury to conduct such modelling, and/or to use any other capable body.

give appropriate representation and support to SMSFs, and be prepared to advocate for them against the interests of large APRA-regulated funds when necessary.

advocate specifically for the very large number of people with quite small superannuation accounts, when their interests are different from those of people with relatively large balances.

The biggest risk to the advocacy body in our view is

that it would over time be hijacked by special interest groups, or hobbled by

its terms of reference. Careful thought

in its establishment, key staffing choices and strong political support would

be helpful to protect against these risks.

Membership issues

Membership of the Body should be part-time, funded essentially per diem and with cost reimbursement only for participation in the information gathering and consumer advocacy processes. A small part-time secretariat could be provided from resources in, say, PM&C or Treasury.

Membership opportunities should be advertised.

Membership of the Body should be strictly limited to individuals or entities that exist purely to advocate for the interests of superannuation fund members. (This would include any cooperative representation of Self-Managed Superannuation Funds.) We would counsel against allowing membership to industry entities which might purport to advocate on behalf of their superannuation fund members, but might also inject perspectives that favour their own commercial interests.

Membership should include individuals with membership in (on the one hand) commercial or industry super funds and (on the other hand) Self-Managed Superannuation Funds. We see no need to ensure equal representation of commercial and industry funds, though we would be wary if representation was only of those in industry funds or only commercial funds.

We offer no view at this stage on whether the Superannuation Consumers Centre would be a useful anchor for a new role, but we would suggest avoiding duplication.

Functions not currently available

The consultation

asks what functions the Consumer Advocacy Body for Superannuation could perform

that are not presently being performed. SOS’s

submission to the Retirement Income Review and earlier submissions on the

changes to retirement income policy that took effect in 2017 shows the range of

superannuation members’ advocacy concerns that are not at present being met.

Prior attempts

to establish consultation arrangements for superannuation members appear to us

to have focussed mostly on the disengagement and limited financial literacy of

some superannuation fund members.

Correctives to those concerns have heretofore looked to financial

literacy education and better access to higher quality financial advice.

Clearly such measures have their place.

But in the view

of Save Our Super, these problems arise in larger part from the complexity and

rapid change of superannuation and Age Pension laws, and in the nature of the

Superannuation Guarantee Charge. Nothing predicts disengagement by customers

and underperformance and overcharging by suppliers more assuredly than

government compulsion to consume a product that would not otherwise be bought

because it is too complex to understand, too often changed and widely

distrusted.

There needs to

be more consumer policy advocacy aimed at getting the policies right, simple,

clear and stable, as was attempted in the 2006 – 2007 Simplified Super reforms.

Other issues

In the time

available, we offer no views on questions 2,3 and 4, which are more for

government administrators.

The Review’s Terms of Reference seek a fact base on

how the retirement income system is working.

This is a vital quest. Such

information, founded on publication of long-term modelling extending over the

decades over which policy has its cumulative effect, has disappeared over the

last decade.

Not coincidentally, retirement income policy has suffered from recent failures to set clear objectives in a long-term framework of rising personal incomes, demographic ageing, lengthening life expectancy at retirement age, weak overall national saving, low household and company saving and a persistent tendency to government dissaving.

A new statement of retirement income policy objectives should be:

to facilitate rising real retirement incomes for all;

to encourage higher savings in superannuation so progressively more of the age-qualified can self-fund retirement at higher living standards than provided by the Age Pension;

to thus reduce the proportion of the age-qualified receiving the Age Pension, improving its sustainability as a safety net and reducing its tax burden on the diminishing proportion of the population of working age; and

to contribute in net terms to raising national saving, as lifetime saving for self-funded retirement progressively displaces tax-funded recurrent expenditures on the Age Pension.

With the actuarial value of the Age Pension to a homeowning couple now well over $1 million, self-funding a higher retirement living standard than the Age Pension will require large saving balances at retirement. It is unclear that political parties accept this. It seems to Save Our Super that politicians champion the objective of more self-funded retirees and fewer dependent on the Age Pension but seem dubious about allowing the means to that objective.

Save Our Super highlights fragmentary evidence from the private sector suggesting retirement income policies to 2017 were generating a surprisingly strong growth in self-funded retirement, reducing spending on the Age Pension as a share of GDP, and (prima facie) raising living standards in retirement (Table 1). (Anyone who becomes a self-funded retiree can be assumed to be better off than if they had rearranged their affairs to receive the Age Pension.) Sustainability of the retirement system for both retirees and working age taxpayers funding the Age Pension seemed to be strengthening. These apparent trends are little known, have not been officially explained, and deserve the Review’s close attention in establishing a fact base.

Retirement policy should be evaluated in a social cost-benefit framework, in which the benefits include any contraction over time in the proportion of the age-eligible receiving the Age Pension, any corresponding rise in the proportion enjoying a higher self-funded retirement living standard of their choice, and any rise in net national savings; while the costs include a realistic estimate of any superannuation ‘tax expenditures’ (this often used term is placed in quotes because it is generally misleading – see subsequent discussion) that reduce the direct expenditures on the Age Pension. Such a framework was developed and applied in the 1990s but has since fallen into disuse.

Policy changes that took effect in 2017 have suffered from a lack of enumeration of the long-term net economic and fiscal impacts on retirement income trends. They also damaged confidence in the retirement rules, and the rules for changing those rules. Extraordinarily, many people trying to manage their retirement have found legislative risk in recent years to be a greater problem than investment risk. Save Our Super believes the Government should re-commit to the grandfathering practices of the preceding quarter century to rebuild the confidence essential for long-term saving under the restrictions of the superannuation system.

Views on whether retirement policy is fair and sustainable differ widely, in large part because the only official analysis that has been sustained is so-called ‘tax expenditure’ estimates using a subjective hypothetical ‘comprehensive income tax’ benchmark that has never had democratic support.

This prevailing ‘tax expenditure’ measure is unfit for purpose. It is conceptually indefensible; it produces wildly unrealistic estimates of hypothetical revenue forgone from superannuation (now said to be $37 billion for 2018-19 and rising); and it presents an imaginary gross cost outside the sensible cost-benefit framework used in the past. It also presents (including, regrettably, in the Review’s Consultation Paper) an imaginary one-off effect as though it could be a recurrent flow similar to the actual recurrent expenditures on the Age Pension.

An alternative Treasury superannuation ‘tax expenditure’ estimate, more defensible because it has the desirable characteristic of not discriminating against saving or supressing work effort, is based on an expenditure tax benchmark. It estimates annual revenue forgone of $7 billion, steady over time, not $37 billion rising strongly.

Additional to the four evaluative criteria proposed in the Consultation Paper, Save Our Super recommends a fifth: personal choice and accountability. Over the 70-year horizon of individuals’ commitments to retirement saving, personal circumstances differ widely. As saving rates rise, encouraging substantial individual choice of saving profiles to achieve preferred retirement living standards is desirable.

We also restate a core proposition perhaps unusual to the modern ear: personal saving is good. The consumption that is forgone in order to save is not just money; it is real resources that are made available to others with higher immediate demands for consumption or investment. Saving and the investment it finances are the foundation for rising living standards. Those concerned at the possibility of inequality arising from more saving should address the issue directly by presenting arguments for more redistribution, not by hobbling saving.

While retirement income ‘adequacy’ is a sensible criterion for considering the Age Pension, ‘adequacy’ makes no sense as a policy guide to either compulsory or voluntary superannuation contributions towards self-funded retirement. Adequacy of self-funded retirement income is properly a matter for individuals’ preferences and saving choices.

The task for superannuation policy in the broader retirement income structure is not to achieve some centrally-approved ‘adequate’ self-funded retirement income, however prescribed. It is to roughly offset the government’s systemic disincentives to saving from welfare spending and income taxing. Once government has struck a reasonable, stable and sustainable tax structure from that perspective, citizens should be entitled to save what they like, at any stage of life.

The Super Guarantee Charge’s optimum future level is a matter for practical marginal analysis rather than ideology. Would raising it by a percentage point add more to benefits (higher savings balances at retirement for self-funded retirees) than to costs (e.g. reduced incomes over a working lifetime, more burden on young workers, or on poor workers who may not save enough to retire on more than the Age Pension)?

The coherence of the Age Pension and superannuation arrangements is less than ideal. Very high effective marginal tax rates on saving arise from the increased Age Pension assets test taper rate, with the result that many retirees are trapped in a retirement strategy built on a substantial part Age Pension. Save Our Super also identifies six problem areas where inconsistent indexation practices of superannuation and Age Pension parameters compound through time to reduce super savings and retirement benefits relative to average earnings. These problems reduce confidence in the stability of the system and should be fixed.

Our analysis points to policy choices that would give more Australians ‘skin in the game’ of patient saving and long term investing for a well performing Australian economy. Those policies would yield rising living standards for all, both those of working age and retirees. Such policies would give more personal choice over the lifetime profile of saving and retirement living standards; fewer cases where compulsory savings violate individual needs, and more engaged personal oversight of a more competitive and efficient superannuation industry.

Terrence O’Brien is an honours graduate in economics from the University of Queensland, and has a master of economics from the Australian National University. He worked from the early 1970s in many areas of the Treasury, including taxation policy, fiscal policy and international economic issues. His senior positions have also included several years in the Office of National Assessments, as resident economic representative of Australia at the Organisation for Economic Cooperation and Development, as Alternate Executive Director on the Boards of the World Bank Group, and as First Assistant Commissioner at the Productivity Commission.

Jack Hammond LLB (Hons), QCis Save Our Super’s founder. He was a Victorian barrister for more than three decades. He is now retired from the Victorian Bar. Prior to becoming a barrister, he was an Adviser to Prime Minister Malcolm Fraser, and an Associate to Justice Brennan, then of the Federal Court of Australia. Before that he served as a Councillor on the Malvern City Council (now Stonnington City Council) in Melbourne.

Jim Bonham (BSc (Sydney), PhD (Qld), Dip Corp Mgt, FRACI) is a retired scientist (physical chemistry). His career spanned 7 years as an academic followed by 25 years in the pulp and paper industry, where he managed scientific research and the development of new products and processes. He has been retired for 14 years has run an SMSF for 17 years.

Sean Corbett has over 25 years’ experience in the superannuation industry, with a particular specialisation in retirement income products. He has been employed as overall product manager at Connelly Temple (the second provider of allocated pensions in Australia) as well as product manager for annuities at both Colonial Life and Challenger Life. He has a commerce degree from the University of Queensland and an honours degree and a master’s degree in economics from Cambridge University.